What exactly happened in the gold market, from its historical high to a single-month plunge of 11.5%?

- April 14, 2026

- Posted by: ACE Markets

- Category: Financial News

In April 2026, one of the most perplexing phenomena in the global financial markets was the unprecedented escalation of the Middle East conflict and geopolitical risks, while gold, widely regarded as the “ultimate safe-haven asset,” experienced an epic plunge. Gold prices fell 11.5% in a single month, marking the largest monthly drop since the 2008 global financial crisis, plummeting over $1,000 from its historical high of over $5,500 per ounce in January. This trend, completely contrary to traditional safe-haven logic, led to unprecedented questioning of gold’s safe-haven status.

A perfect storm of multiple factors

The plunge in gold prices was not caused by a single factor, but rather by a combination of factors including a short-term liquidity crisis, previous market overheating, expectations of a shift in monetary policy, and sudden changes in central bank behavior.

1. The liquidity drain effect in the early stages of the crisis

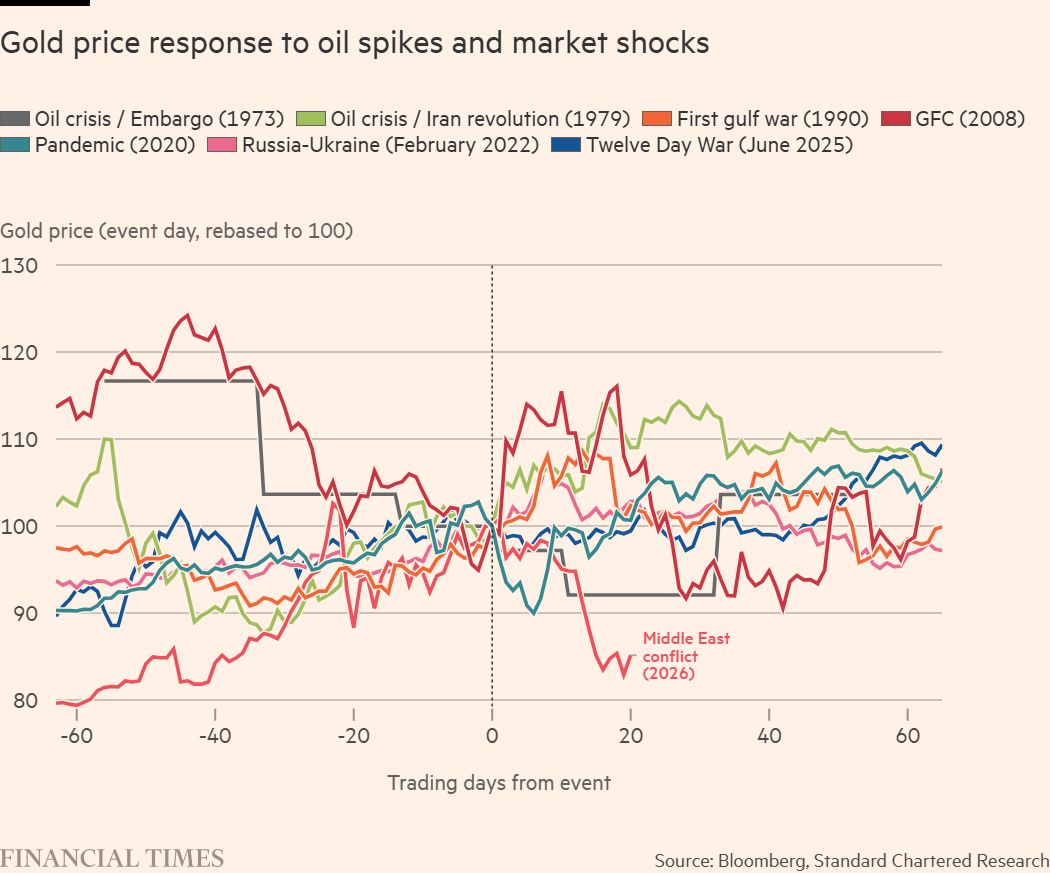

Standard Chartered’s Suki Cooper points out that gold is often sold off in the early stages of a crisis due to liquidity needs—when stock market declines trigger margin calls, gold, with its high liquidity and significant prior gains, becomes a prime target for selling. Historically, liquidity pressures typically suppress gold prices for 4-6 weeks after a crisis; during the 2008 financial crisis, it took gold more than four months to recover its losses. Following this conflict, implied volatility for gold surged to pandemic levels and quickly shifted from its most overbought state since 1999 in January to its most severely oversold state since 2013, further amplifying the decline.

2. Cooling expectations of a US interest rate cut severely impact gold prices.

There is a very strong negative correlation between gold and US real interest rates. Since gold does not generate dividends or interest, the opportunity cost of holding gold increases when interest rates rise, and gold prices tend to fall. This correlation was temporarily broken at the end of 2022 due to large-scale gold purchases by central banks, but in recent weeks, with US inflation data exceeding expectations and market expectations for a Federal Reserve rate cut this year cooling significantly, the traditional relationship between gold and interest rates has re-emerged.

3. The central bank’s sell-off became the final straw.

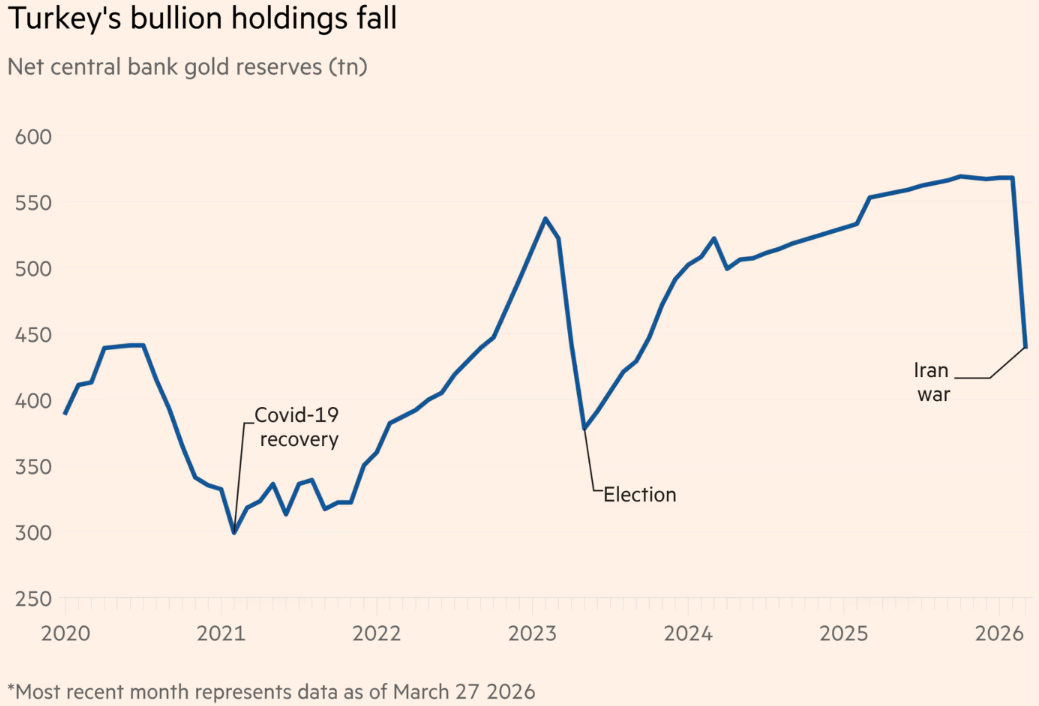

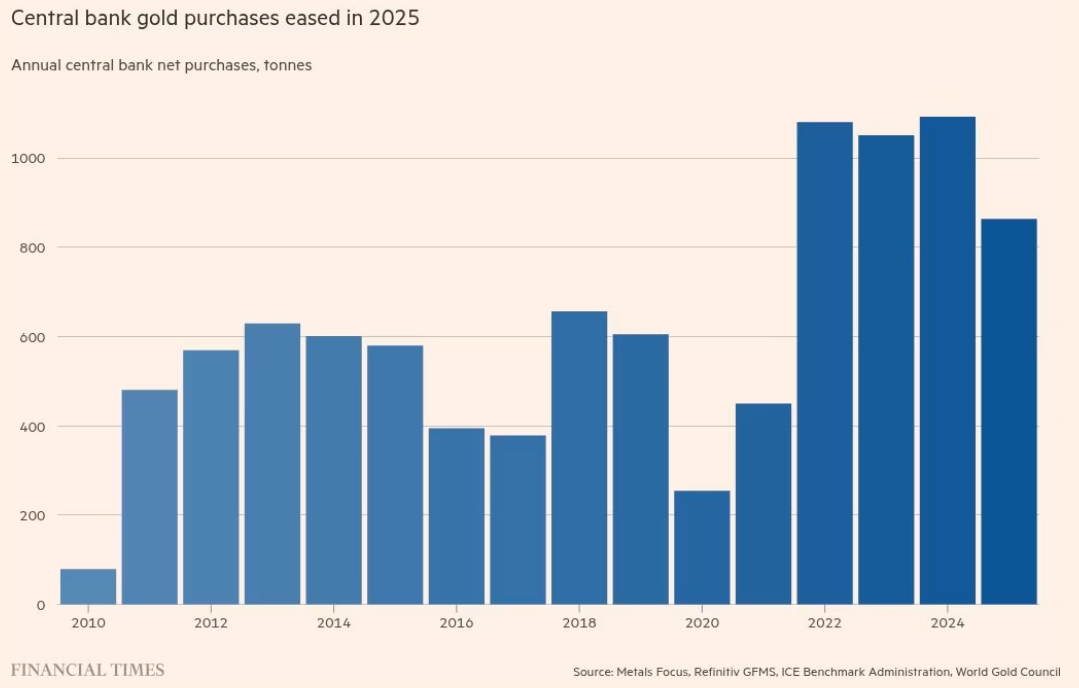

The large-scale sell-off by some central banks was the direct trigger for the gold price crash. Following the outbreak of the Iran-Iraq War, Turkey sold or lent out $20 billion worth of gold. According to Metals Focus data, from February 27 to March 27, Turkey net sold 52 tons and arranged 79 tons of gold swap transactions, reducing its gold reserves to 440 tons, the lowest in over two years, in an effort to support its currency and curb 31% inflation. Furthermore, Russia sold 15 tons of gold in January and February this year, and the governor of the Polish central bank proposed selling gold to raise defense funds, raising market concerns that countries like India might follow suit. Previously, central banks were the core drivers of the gold bull market, with global central bank net purchases of gold reaching a record high of 863 tons in dollar terms by 2025. This shift in behavior broke market expectations and triggered a panic sell-off.

Divergent central banks and unchanged safe-haven status

It’s worth noting that global central banks’ attitudes towards gold are not monolithic, but rather show a clear divergence. While some countries are selling off their gold reserves, others are steadily increasing their holdings. The People’s Bank of China’s gold reserves stood at 74.38 million ounces at the end of March, an increase of 160,000 ounces from the end of February. This marks the 17th consecutive month of increases by the People’s Bank of China and the largest single purchase reported in over a year. France, meanwhile, has completed its years-long gold withdrawal plan, no longer holding any gold in the United States, reflecting the growing emphasis placed on the security of gold reserves by various countries.

Despite the recent sharp decline, many analysts believe that gold’s safe-haven status remains unshaken, and its long-term upward trend remains intact. Gold can play both a leading and supporting role in the market, but this doesn’t mean it has lost its traditional functions. Historical experience shows that once liquidity pressures ease, investors will resume increasing their gold holdings. Currently, the sell-off of ETPs has begun to slow, indicating that previously overheated positions may have been largely cleared out.

From a fundamental perspective, current gold prices do not fully factor in two core risks:

- Economic recession risk : During economic recessions, gold typically rises by an average of 15%, while industrial commodities are dragged down by declining output.

- Stagflation risk : Even if the Middle East conflict ends tomorrow, oil prices are likely to remain high for longer, exacerbating concerns about rising inflation. As a store of value, gold typically performs strongly in environments of rising inflation.

Furthermore, many structural drivers for gold remain robust, including concerns about high US and global debt, fiat currency depreciation, tariff and trade uncertainty, and geopolitical risks. Technically, the 200-day moving average has provided strong support for gold since October 2023, a level it has never breached.

Three key indicators for future focus

In the short term, the gold market will continue to face challenges from liquidity pressures and uncertainty surrounding central bank actions, making its price movement difficult to predict linearly. However, in the medium to long term, the probability of gold prices resuming their upward trend remains relatively high. Investors should focus on the following three key indicators:

- ETP Fund Flows : ETP investors are more focused on actual yield expectations, and their fund flows are an important indicator of short-term market sentiment.

- Central bank gold purchase trends : Whether central banks will continue to sell gold, and the extent to which major buyers such as China increase their holdings, will have a decisive impact on gold prices.

- US interest rate policy : The timing and magnitude of the Federal Reserve’s interest rate cuts will directly determine the opportunity cost of holding gold.

This sharp drop in gold prices is not the demise of the safe-haven myth, but rather a temporary phenomenon occurring in the unique market environment at the beginning of a crisis. As has been proven by every major crisis in history, once the dust settles, gold will remain an indispensable cornerstone of investors’ portfolios.