From supply disruption panic to ample supply: a deep game played in the rapid shift of the crude oil market

- July 7, 2026

- Posted by: ACE Markets

- Category: Financial News

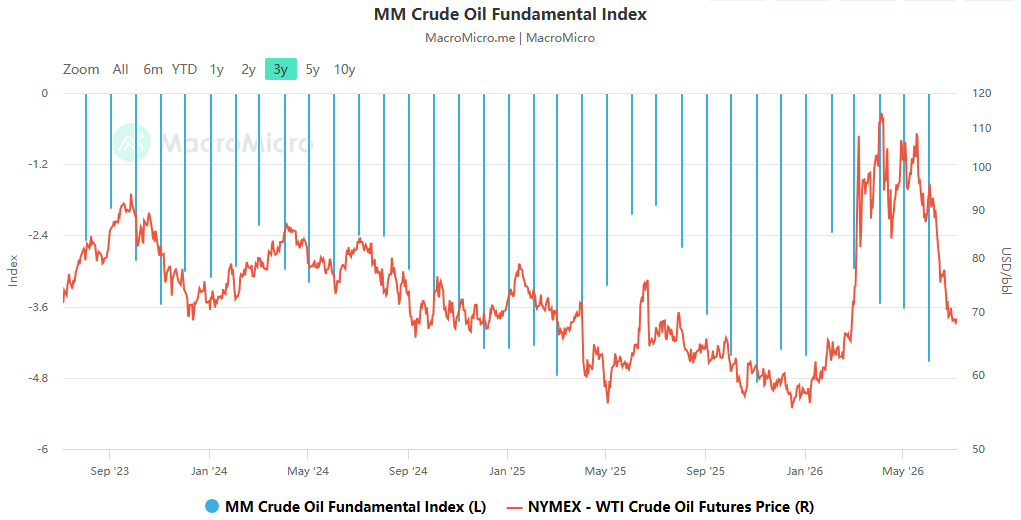

In just a few weeks, the international crude oil market has undergone a dramatic shift from “supply disruption anxiety” to “oversupply expectations.” Saudi Aramco’s largest price cut for Asian crude oil in 26 years, the gradual resumption of shipping in the Strait of Hormuz, and OPEC+’s continued efforts to increase production have all contributed to a decline in Brent crude oil prices back to pre-conflict levels seen at the end of February. ACE Markets’ commodity research team, relying on its crude oil supply and demand balance monitoring framework, inventory cycle calculation model, and geopolitical game analysis system, combined with high-frequency data from the Strait of Hormuz shipping, global inventory changes, and regional situation dynamics, has made a comprehensive assessment: the current loose supply situation in crude oil is basically established, and short-term oil prices still face downward pressure; however, the structural contradiction of historically low global inventories remains unresolved, and the long-term nature of inventory repair is reshaping the power balance in the US-Iran geopolitical game. Coupled with local security risks in the Red Sea and other regions, the potential for a deep market decline is also limited.

Ample supply quickly materializes: Saudi Arabia’s price war kicks off a battle for market share.

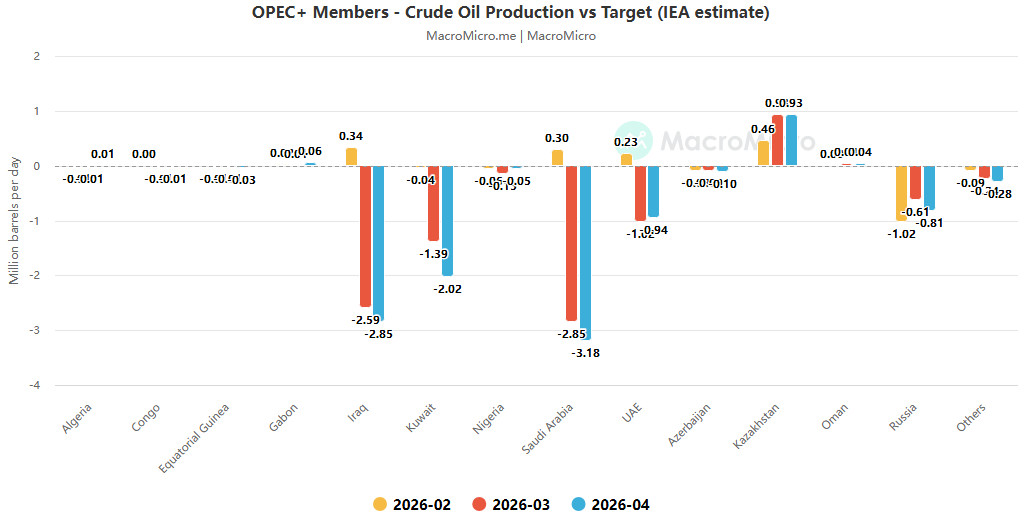

The core driver of this round of oil price reversal is that the speed of supply-side recovery has significantly exceeded market expectations. With the ceasefire agreement reached between the US and Iran and the gradual reopening of the Strait of Hormuz, crude oil production capacity previously hampered by the blockade has been rapidly released. ACE Markets shipping monitoring data shows that current Persian Gulf crude oil shipments have doubled since May, with shipments from Saudi Arabia’s Ras Tanura port recovering to approximately 90% of pre-war levels. Exports from the UAE, Kuwait, and other countries are also continuing to rebound, and overall regional supply has largely covered the gap caused by the conflict.

As supply recovers, Saudi Arabia has spearheaded a price war in the Asian market. Saudi Aramco lowered its official selling price for Arab Light crude oil to Asia by $11 per barrel in August, a discount of $1.5 per barrel to the regional benchmark. This is the largest price reduction in at least 26 years, significantly exceeding the market’s previous expectation of an $8 decrease. ACE Markets analysts believe this price cut is both a passive response to weakening spot prices and a proactive strategy to seize market share during a period of ample supply—as Middle Eastern crude oil flows back to Asia, major oil-producing countries need to secure refinery orders through price advantages.

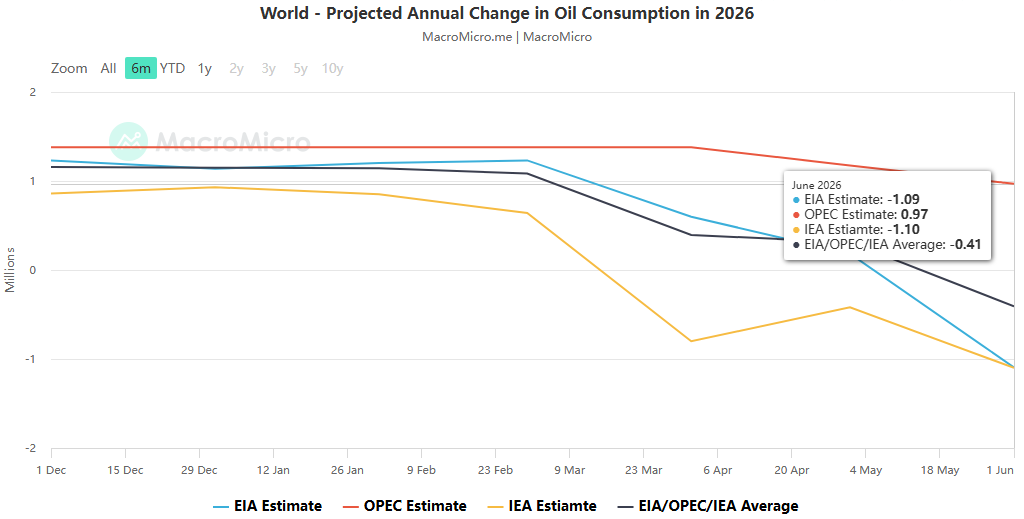

OPEC+’s production increase policy has further reinforced expectations of further easing. The organization has been pushing forward with its production cut exit for the fifth consecutive month, with a planned increase of 188,000 barrels per day in August. Unlike previous instances where increased production was merely symbolic due to shipping disruptions, with transportation channels now open, Saudi Arabia, Iraq, Kuwait, and other countries can fully utilize their additional quotas, and the actual increase in supply will gradually materialize. Weak demand amplifies the perception of ample supply. Major Asian importers have not yet significantly increased their purchases, and the lack of sufficient buying interest to absorb the new supply has directly driven down spot prices: Oman crude oil spot prices were once at a discount of about $4 to the Dubai benchmark, hitting their lowest level since the pandemic; the term structure for Brent and Dubai crude oil has shifted to a premium for futures, reflecting the market’s pricing of a short-term oversupply.

The core contradiction beneath the veneer of loose monetary policy: delayed inventory repair reshapes geopolitical leverage.

While a short-term supply easing is widely acknowledged, ACE Markets’ inventory cycle model monitoring shows that the recovery of global crude oil inventories is severely lagging, representing the most easily overlooked structural contradiction in the current market. Data shows that OECD member countries’ crude oil inventories decreased by a cumulative 163 million barrels from March to May, reaching their lowest level since December 1990; the US Strategic Petroleum Reserve (SPR) is at a historical low since 1983, facing immense pressure to replenish its reserves but with a slow pace of progress.

The long-term nature of inventory repair is profoundly altering the balance of power in the US-Iran rivalry. Historical calculations show that even at a rate of 200,000 barrels per day, replenishing the US Strategic Petroleum Reserve would take 15-18 months to return to pre-conflict levels. Currently, US policy remains focused on suppressing oil prices, lacking the incentive for large-scale inventory replenishment, potentially extending the overall inventory rebuilding cycle to 2027. ACE Markets’ geopolitical analysis system suggests that Iran previously held the upper hand in negotiations by “blockading the Strait of Hormuz and threatening global energy supplies,” but this core bargaining chip has been significantly weakened with the resumption of shipping and the decline in oil prices. Furthermore, the 60-day negotiation window, far shorter than the inventory repair cycle, gives the US a more proactive stance in subsequent negotiations.

The divergence between bulls and bears intensifies: downward pressure and tail risks coexist.

The interplay of ample supply and low inventory levels has significantly amplified market divergence regarding the future trajectory of oil prices. Bears believe that with weak demand recovery and inventory buying yet to begin, short-term oversupply will continue to suppress oil prices, with institutions like Citigroup predicting Brent crude could fall to $60 per barrel by the end of the year. However, ACE Markets argues that the support for the sharp price drop is equally clear: global inventories are at historically low levels, and prices could easily rebound once demand recovers marginally or supply fluctuates; furthermore, OPEC+ retains room for policy flexibility, and if oil prices fall more than expected, it cannot be ruled out that production increases could be suspended or even production cuts could be restarted, forming a policy floor.

Tail risks should not be ignored either. Although the Strait of Hormuz is gradually reopening to navigation, mines remain in the central waters, and security risks have not been completely eliminated. Institutions such as the Royal Bank of Canada predict that transit volumes through the strait will continue to be lower than pre-war levels. Furthermore, recent attacks on cargo ships in the Red Sea reflect the continued uncertainty surrounding Houthi and other proxy forces, and localized shipping disruptions could trigger short-term oil price fluctuations at any time. ACE Markets believes that the market has already fully priced in optimistic expectations of a ceasefire and supply recovery, but has under-priced in the fragility of the regional situation, and the risk premium is unlikely to disappear completely.

Market Outlook and Key Tracking Directions

ACE Markets assesses the future trend of the crude oil market by considering three key dimensions: supply and demand, inventory, and geopolitics.

- Price Trends : In the short term, driven by ample supply and weak demand, oil prices may still decline further, with the $60-65/barrel range providing dual support from strategic restocking demand and policy support. In the medium term, as inventories are gradually rebuilt and demand recovers marginally, oil prices are expected to stabilize and rebound, with limited room for a significant drop.

- Geopolitical landscape : The deterrent effect of blocking the Strait of Hormuz has significantly decreased, and the US has gained more say in the US-Iran negotiations, but the regional situation remains fragile, and localized attacks may repeatedly disrupt market sentiment.

- Policy direction : OPEC+ will maintain a pace of “cautious production increases + flexible adjustments,” dynamically adjusting its production policy according to oil price trends, thus becoming an important support force for oil prices.

ACE Markets will continue to track four core dimensions: the progress of shipping recovery in the Strait of Hormuz and changes in oil-producing countries’ exports, the adjustment of OPEC+ production policies, the pace of replenishment of global commercial inventories and strategic reserves, and the evolution of the security situation in the Red Sea and the Persian Gulf, in order to promptly capture market turning points and risk signals.