Trump’s policy shift is driving oil price volatility, and commodity funds are experiencing record outflows

- March 30, 2026

- Posted by: ACE Markets

- Category: Financial News

ACE Markets leverages its geopolitical risk monitoring system, energy price tracking model, global ETF fund flow database, and cross-asset stress transmission model to conduct comprehensive analysis of global energy and financial markets and capital flows amid the Middle East conflict. The core logic of the current market has fundamentally shifted: the Trump administration’s policy statements are constrained by multiple “pain points,” including oil prices, inflation, US Treasury yields, and public opinion, with its social media rhetoric becoming a key driver of oil price volatility. Simultaneously, global commodity ETFs have experienced their largest monthly outflows since records began in 2005, completely reversing the safe-haven asset logic. Gold has seen massive redemptions, while crude oil has diverged against the trend, and the market has entered a phase of extreme volatility and a breakdown in expectations. ACE Markets, through multi-dimensional data cross-validation, has captured market reversal signals in advance, clarifying the core drivers and risk boundaries of this round of volatility for investors.

Trump’s policy statements are subject to multiple constraints, with “verbal intervention” dominating the dramatic fluctuations in oil prices.

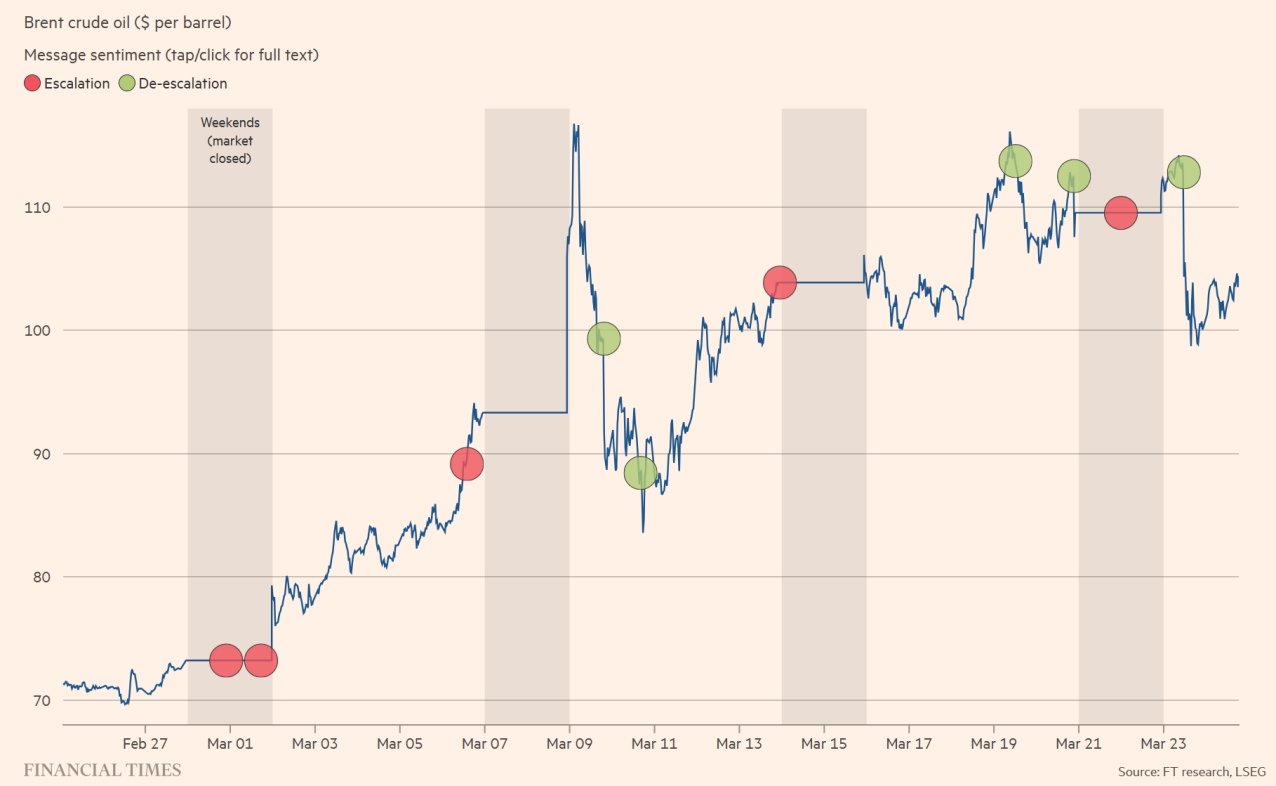

ACE Markets energy market monitoring data shows that since the escalation of the conflict with Iran, Trump’s policy statements have exhibited a clear pattern: escalating threats against Iran during weekend market closures and releasing peace signals when oil prices surge. The core objective is to curb gasoline price inflation and avoid pressure from midterm election voters. This pattern confirms the crucial influence of the oil market on White House policy and demonstrates the effectiveness of current “verbal intervention” in controlling oil prices.

The platform’s analysis strongly aligns with the views of Onyx Capital analysts: high gasoline prices are a core political risk for the Trump administration. As oil prices approach $95-100 per barrel, conciliatory rhetoric from the White House is bound to intensify. Brent crude once touched $119 per barrel, and the sharp rise in US gasoline and diesel prices has already had a substantial impact on US consumers and businesses. Although traders believe that oil prices should be even higher due to the impact of the conflict, they are wary of White House interference and dare not short the market, resulting in a unique market pricing pattern. ACE Markets’ cross-asset stress model simultaneously validates this, showing that US borrowing costs have risen to a near 12-month high, the 10-year US Treasury yield has risen sharply this month, and oil price-driven inflation has cooled expectations of a Fed rate cut, further tightening financial conditions.

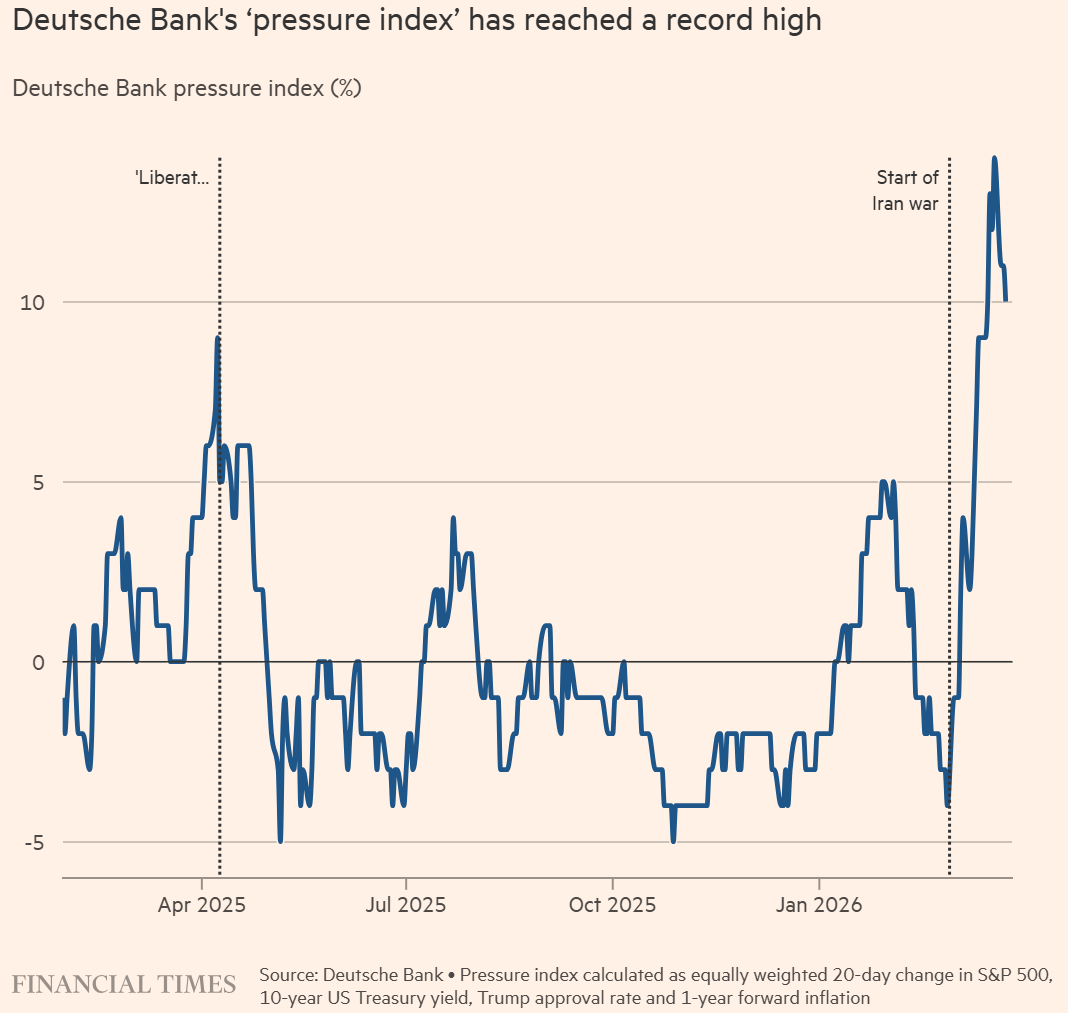

Deutsche Bank’s US Policy Pressure Index has reached a record high. This index encompasses four core indicators: the S&P 500, US Treasury yields, Trump’s approval rating, and inflation expectations. A rising index significantly increases the probability of government policy adjustments, perfectly aligning with ACE Markets’ policy shift prediction. Amundi’s research view also agrees with the platform: when the 10-year US Treasury yield approaches 4.5%, the White House has a strong incentive to shift policy, and investors need to anticipate this key threshold. Currently, market expectations are highly confused, with the Trump administration simultaneously releasing contradictory signals regarding military escalation, peace negotiations, and reserve requirement ratio cuts, leading to a wait-and-see attitude on Wall Street. ACE Markets suggests that the market is closely watching the next “policy shift moment,” and amidst the interplay of rhetoric and physical supply and demand, oil prices will likely remain highly volatile in the short term.

Commodity ETFs saw record outflows, gold was sold off, and crude oil funds diverged against the trend.

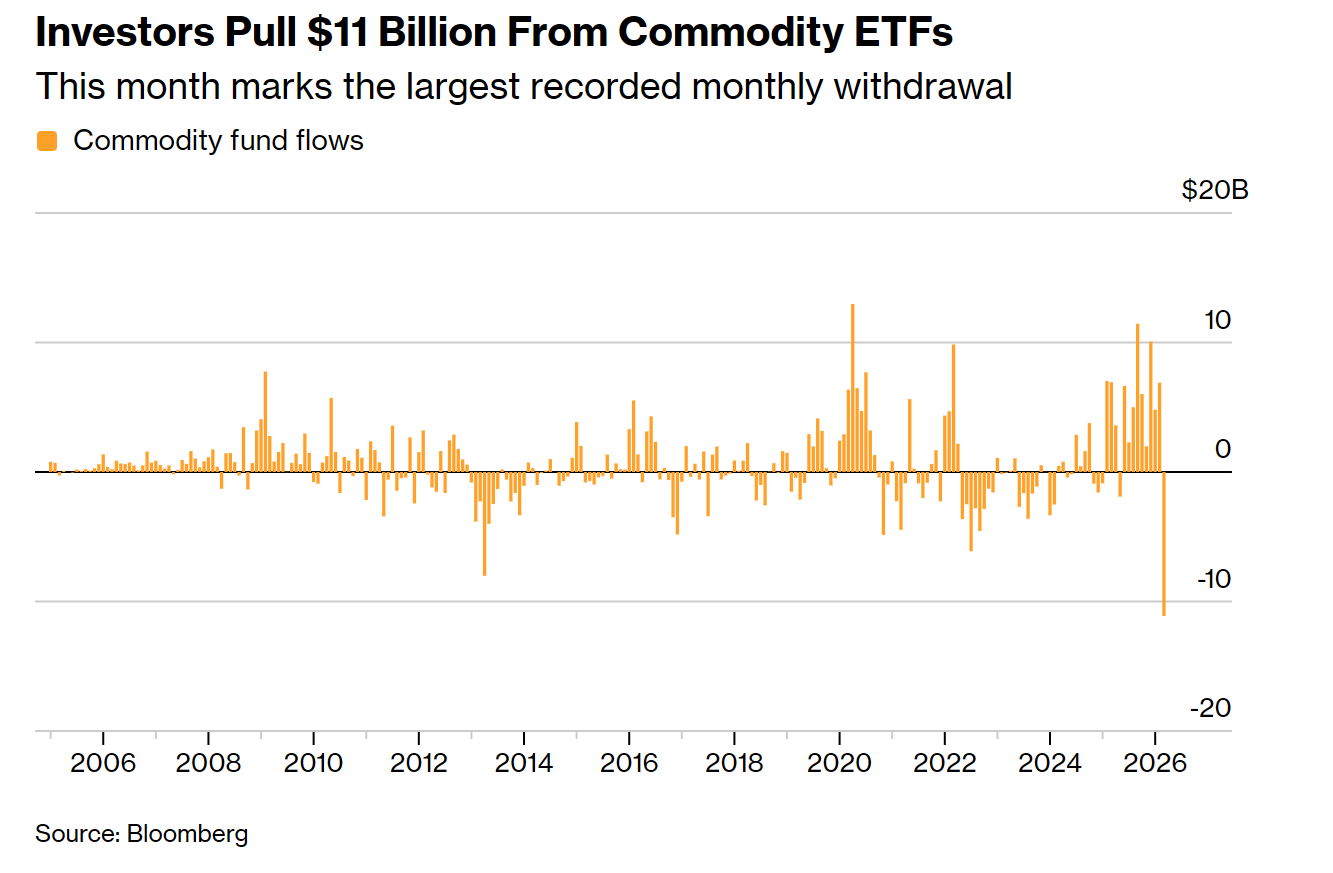

ACE Markets’ global ETF fund flow monitoring system captured a landmark fund flow anomaly: global commodity ETFs saw a single-month outflow of $11 billion in March, the largest amount since records began in 2005, completely reversing the previous nine-month inflow trend and rendering the traditional logic of safe-haven assets completely ineffective. This round of outflows showed a significant structural divergence: precious metals became the main force of the sell-off, with the world’s largest gold ETF (GLD) experiencing redemptions of over $7 billion, and silver ETFs seeing outflows of $1.4 billion; oil ETFs, on the other hand, bucked the trend and attracted funds, with the US Oil Fund (USO) attracting approximately $400 million in a single month, and Brent crude oil holding steady above $104 per barrel, indicating a complete divergence between energy and metal price movements.

ACE Markets analysis points to three core reasons for this round of capital reversal: First, gold’s previous surge led to panic selling and profit-taking; second, high interest rates and expectations of a strong dollar continued to suppress the attractiveness of non-interest-bearing precious metals; and third, geopolitical instability has led the market to prioritize cash, with investors selling highly liquid, profitable positions for cash. This assessment resonates strongly with the views of Bloomberg Industry Research and DeCarley Trading analysts, who believe the market is currently in a state of extreme dysfunction, with metal buyers experiencing “buyer’s regret” and a severe disconnect in capital expectations.

ACE Markets’ Key Outlook

ACE Markets, based on a comprehensive analysis of geopolitical, energy, capital, and macroeconomic data, believes that short-term market volatility will primarily depend on the Trump administration’s policy statements. The Deutsche Bank Stress Index, the 10-year US Treasury yield, and gasoline prices are three key signals for judging policy shifts. Divergence in commodity funding will continue, with crude oil maintaining high volatility supported by geopolitical supply and demand, while gold still faces adjustment risks under pressure from high interest rates and capital outflows. Investors should rely on ACE Markets’ real-time monitoring system to closely monitor White House statements, shipping conditions in the Strait of Hormuz, and marginal changes in ETF fund flows, and be wary of cross-asset volatility risks triggered by unexpected policy shifts and the resonance of oil prices and US Treasury yields.

This article is based on cross-validation of data from multiple models including ACE Markets’ global geopolitical monitoring, energy tracking, and fund flow analysis, and does not constitute investment advice. Geopolitical conflicts, policy interventions, and inflation expectations all have the potential for unexpected changes, increasing market volatility. Investors need to manage their positions and risks accordingly.