The suspense of easing amid contradictory data: Fed rate cut expectations and Powell’s key statement

- August 20, 2025

- Posted by: ACE Markets

- Category: Financial News

Currently, global markets are focused on the Federal Reserve’s policy direction, particularly the upcoming September meeting and Chairman Powell’s speech at the Jackson Hole Economic Policy Symposium. Economic data, including employment and inflation, paint a complex picture, with significant divergence among institutions and analysts regarding the timing and magnitude of any rate cuts. The market’s balancing act between expectations for easing policy and potential risks is intensifying.

The tug-of-war between a cooling labor market and sticky inflation

Recent economic data paints a conflicting picture. Regarding employment, the non-farm payroll report released in early August showed that the three-month average of new jobs fell to its weakest level since 2010, with data for June and May significantly revised downward, highlighting signs of a slowing labor market. However, initial jobless claims remained low, suggesting continued resilience in the labor market. More notably, St. Louis Fed President Alberto Musallem noted that negative job growth does not necessarily indicate a loose labor market. Furthermore, with immigration nearing stagnation, “break-even job growth may even have fallen to near zero,” further complicating the interpretation of labor market dynamics.

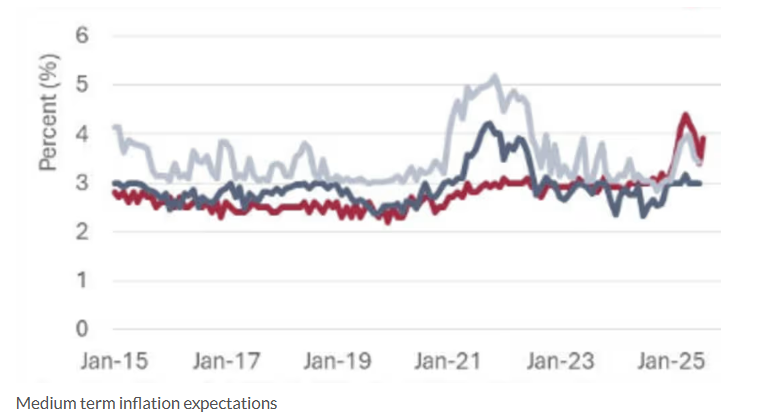

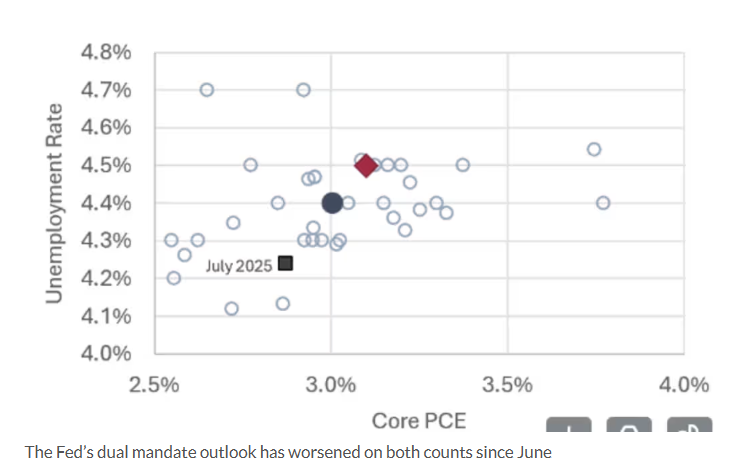

Inflation data complicates policymaking. Last week’s unexpected surge in the Producer Price Index (PPI) and relatively mild readings in the Consumer Price Index (CPI) have together reignited the debate over sticky inflation. The Federal Reserve’s preferred inflation measure, the core Personal Consumption Expenditures (PCE) price index, is projected to reach an annualized rate of 3.1% in the fourth quarter. A Philadelphia Fed survey of professional forecasters indicates a median year-on-year inflation growth rate of 3% in the fourth quarter of 2025, both well above the Fed’s official 2% target. Furthermore, retail sales data met strong expectations, demonstrating continued consumer resilience, further increasing uncertainty about a decline in inflation. This situation of a cooling labor market without stalling and persistent sticky inflation has worsened the outlook for the Fed’s dual mandate (price stability and maximum employment) since last June and posed a dilemma for any interest rate cuts.

The game of timing and magnitude of interest rate cuts

Faced with complex data, different institutions and analysts have shown clear differences in their judgment on the Fed’s interest rate cut path.

Goldman Sachs is more optimistic, arguing that weak job growth and concerns about downward data revisions have prompted the Federal Reserve to resume rate cuts. Its report predicts that the labor market will remain “mediocre” due to factors such as slowing economic activity, White House staff reductions, and tightened immigration enforcement. Coupled with the economic uncertainty caused by tariffs, the Fed is likely to cut interest rates by 25 basis points each in September, October, and December, and two more cuts next year. If the unemployment rate rises significantly or the employment data worsens, a single 50 basis point cut is not ruled out.

Barclays, however, took a cautious approach, emphasizing that Powell’s “wait-and-see” stance remains elusive, and that hawkish members of the Federal Open Market Committee (FOMC) have shown no signs of backing off. Therefore, a September rate cut remains “up in the air,” and the bank maintains its forecast for only one rate cut this year, in December. The bank noted that Powell’s speech is crucial: if he reiterates his wait-and-see stance, expectations for a September rate cut could be tempered; if he emphasizes labor market weakness, expectations for a rate cut could be reinforced.

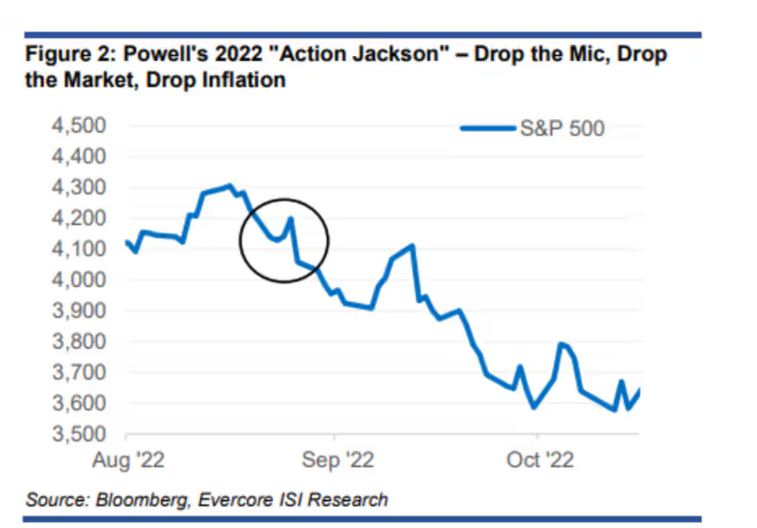

Furthermore, Julian Emanuel, chief strategist at Evercore ISI, warned that market expectations for Powell to deliver a dovish signal risk being dashed. He noted that the S&P 500’s current forward price-to-earnings ratio has risen to 25.5, its highest level since 2000, and is about to enter a period of seasonal weakness. If Powell only hints at a 25 basis point rate cut in September and rules out a 50 basis point, the market could face a short-term correction of 7%-15%. This echoes the precedent of Powell’s hawkish stance at the 2022 Jackson Hole conference, which triggered a sharp stock market sell-off.

Market expectations and key event outlook

The market has already fully priced in a rate cut: According to the CME FedWatch tool, the probability of a 25 basis point rate cut at the September 16-17 meeting is just under 85%. However, all parties agree that two major events this week will determine expectations: the release of the minutes from the July policy meeting early Thursday morning, and Powell’s speech at Jackson Hole on Friday. Most analysts believe Powell’s speech will maintain a cautious tone, emphasizing “moderate” and “gradual” progress, defending the Fed’s independence, and that the policy path will remain data-driven. A hawkish tone could dampen expectations for a September rate cut; a dovish signal could strengthen market confidence in easing.

Regardless, amidst complex economic data and diverging institutional perspectives, market deliberation over the Fed’s policies will continue, increasing the risk of short-term volatility in both the stock and bond markets. For investors, strategies recommended by Evercore ISI—such as buying put options on the Nasdaq 100 Index, investing in reasonably valued sectors like healthcare, and reducing holdings of overvalued stocks—may reflect the market’s current caution regarding the risk of an “autumn correction.” The Fed’s ultimate policy decision will require further economic data and time to determine.