The data game triggered by the shutdown: Decoding the “paradox” of the US labor market

- November 10, 2025

- Posted by: ACE Markets

- Category: Financial News

The ongoing shutdown of the U.S. federal government has not only disrupted the release schedule of official economic data but has also plunged the already adjusting labor market into a “data fog.” The absence of official employment and inflation data has forced markets and policymakers to turn to private sector alternative data for clues. However, these statistics from different institutions present contradictory pictures—a wave of layoffs coexisting with a rebound in employment, and a slowdown in hiring intertwined with stable wages. This highlights the complexity of the labor market and puts the Federal Reserve’s policy decisions in a dilemma.

Since the government shutdown on October 1st, the U.S. Bureau of Labor Statistics (BLS) has not released core employment reports such as the unemployment rate and non-farm payrolls for two consecutive months, making alternative data a “lifeline.” Andrew Hasby, an economist at BNP Paribas, warned that even if businesses reopen, the October data may be distorted due to its reliance on retrospective surveys, or even be unavailable. Inflation data such as the CPI, which relies on in-person surveys, have also stalled, yet this data is crucial for balancing inflation and the labor market. Faced with this data gap, the Federal Reserve and other regulators have had to rely on private indicators such as the Challenger layoff statistics and ADP employment data, but differences in statistical methods have created difficulties in interpretation.

Paradoxical Alternative Data: The Labor Market Presents a Mixed Landscape

The labor market, as presented by private sector data, is a mixed bag. Layoff alarms continue to sound. A report by Challenger, Gray & Christmas shows that U.S. companies announced 153,074 layoffs in October, nearly double the number announced in September. Key reasons include cost-cutting and the accelerated adoption of artificial intelligence. As of October, the total number of layoffs this year has exceeded 1,099,500, a 65% increase compared to the same period last year, marking the highest level for the same period since the COVID-19 pandemic began in 2020.

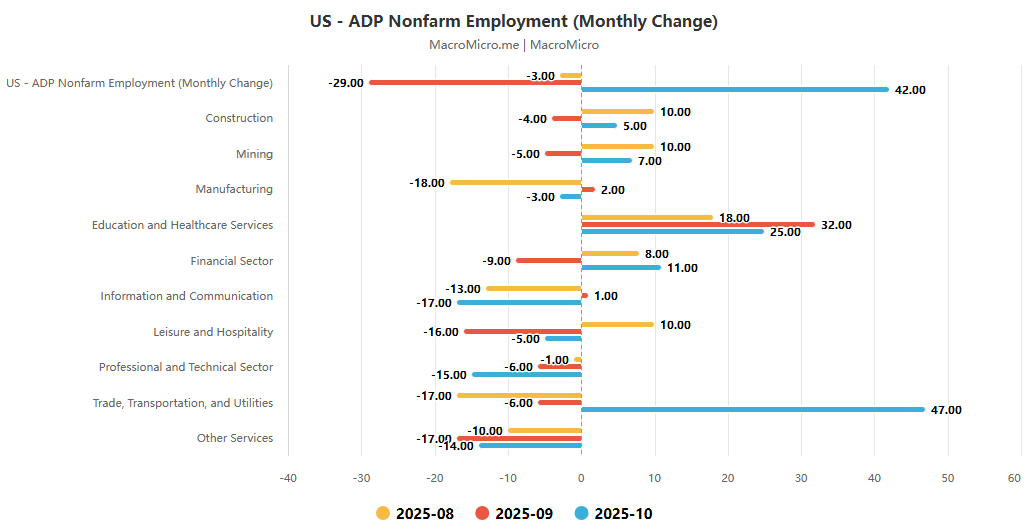

In contrast to the wave of layoffs, there has been a partial rebound in employment. Data from payroll processing company ADP shows that the U.S. private sector added 42,000 jobs in October, the largest increase since July 2025, reversing the decline of the previous two months. Education, healthcare, and trade/transportation/utilities were the main drivers of growth, with trade/transportation/utilities adding 47,000 jobs in a single month, demonstrating the resilience of some industries. Wage growth also remained stable, with the median annual wage growth rate in most industries remaining in the range of 4.2%-5.2%. ADP Chief Economist Nela Richardson pointed out that wage growth has been basically flat for more than a year, reflecting that the supply and demand of labor remains in a relatively balanced state.

The job market exhibited a mixed pattern of “overall weakness with some localized strength.” Data from the job search website Indeed showed that the number of job postings at the end of October fell to its lowest level since February 2021, with almost all industries experiencing year-on-year declines. The declines were particularly pronounced in states like Washington and California, which have a high concentration of technology and government jobs. However, demand for healthcare, engineering, and some field-operational technical positions remained strong. LinkedIn data also showed that the month-on-month decline in job postings in October (0.8%) was significantly narrower than in September (3.5%), suggesting that the slowdown in hiring may be moderated.

The unemployment rate, however, remained relatively stable. The Chicago Federal Reserve estimated the October unemployment rate at 4.36%, almost unchanged from September’s 4.35%, continuing its previous low trend. Economists analyze that the tightening of immigration policies, leading to a reduction in the available labor supply, is a key reason why the unemployment rate did not rise sharply despite increased layoffs.

Contradictory Signal Transmission: Multiple Responses from Policy, Market, and Entities

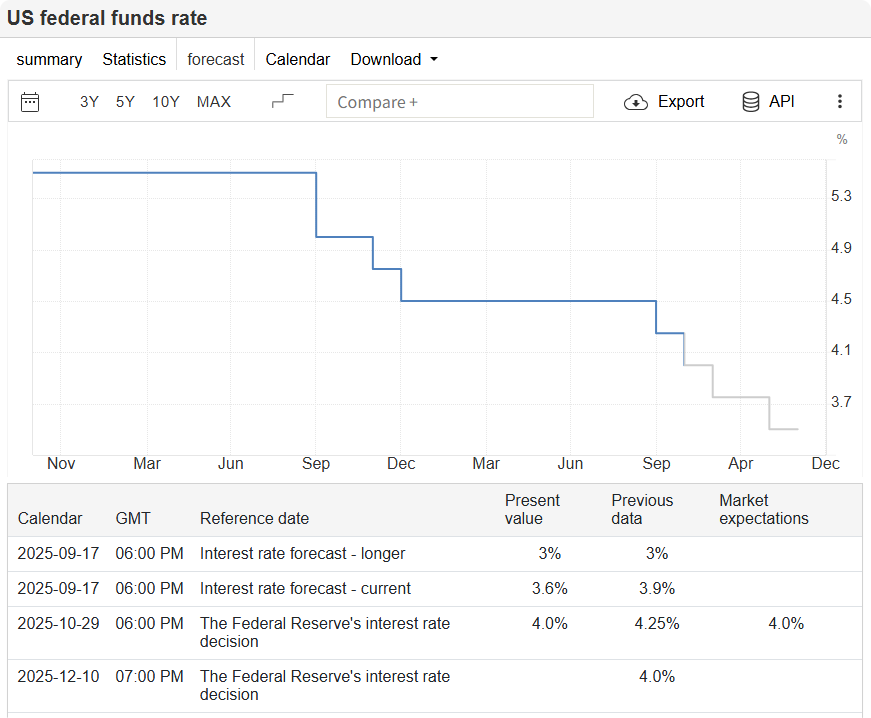

The contradictory signals from the labor market have directly exacerbated policy divisions within the Federal Reserve. The Fed already cut interest rates by 25 basis points at its October meeting, but Chairman Powell made it clear that another rate cut in December would be “no easy task.” Those supporting rate cuts cite weak ADP employment growth and declining job postings as evidence of downside risks in the labor market; those opposing rate cuts, on the other hand, emphasize the continued need to be vigilant about inflation risks, citing a stable unemployment rate, steady wage growth, and low unemployment claims.

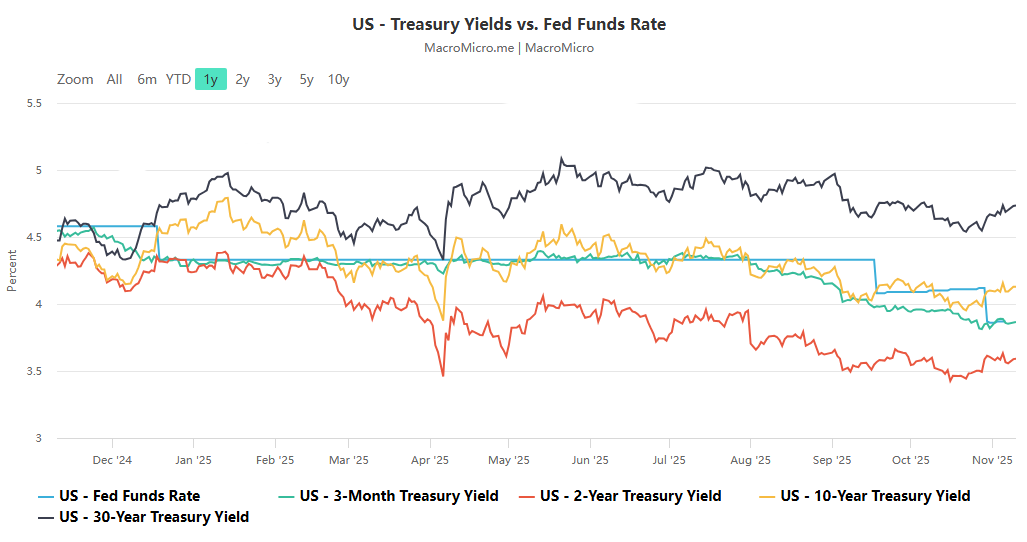

The market is equally sensitive to conflicting data. Following the ADP report, spot gold briefly fell $4 before rebounding quickly, while the dollar index rose slightly by 7 points. Meanwhile, during the alternating release of layoff and employment data from different institutions, yields in the $29 trillion US Treasury market fluctuated in different directions, leaving investors in a dilemma due to the lack of a unified “gold standard” data. Ed Al-Husseini, portfolio manager at Threadneedle Investment in Colombia, stated bluntly that unemployment insurance claims and the official unemployment rate remain irreplaceable core indicators, and the contradictions in alternative data highlight the market’s collective predicament.

Businesses and workers are also adapting to this uncertainty. Gregory Daco, chief economist at EY, points out that whether due to weak demand, rising costs, or technological substitution, reduced demand for talent has become a “future reality.” Glassdoor’s employee confidence index fell to its lowest point since June in October, reflecting workers’ concerns about job security in a market with limited external choices.

Future Direction: Data Clarification and Structural Adjustment are Key

Currently, the market still bets on a greater than 50% probability of a Fed rate cut in December, but this expectation is highly dependent on subsequent data for clarification. If official data released after the government shutdown ends shows a significant weakening of the job market, it could provide support for a rate cut; if the data confirms the resilience of some sectors or reveals emerging inflationary pressures, it could lead to a more cautious policy shift.

For the labor market, the trend of structural adjustment has become increasingly clear. The application of artificial intelligence and the need for corporate cost control will continue to put pressure on white-collar jobs; while the resilience of demand in counter-cyclical industries such as healthcare and physical operational technical jobs may act as a “stabilizer” for the job market. However, if the wave of layoffs spreads from the current concentrated areas to a wider range, and the recruitment market fails to absorb it in time, the previously low unemployment rate may face upward pressure.

This data crisis triggered by the government shutdown has also exposed the fragility of the US economic monitoring system. Once the credibility of official data is damaged, rebuilding market confidence will take much longer. In any case, until the data gaps are closed, contradictory signals from the labor market will persist, and the Federal Reserve’s policy decisions, corporate hiring and layoff plans, and workers’ career choices will all proceed cautiously amidst this uncertainty.