Gold suffered its biggest weekly drop in over 40 years. What was the core driver behind this?

- March 25, 2026

- Posted by: ACE Markets

- Category: Financial News

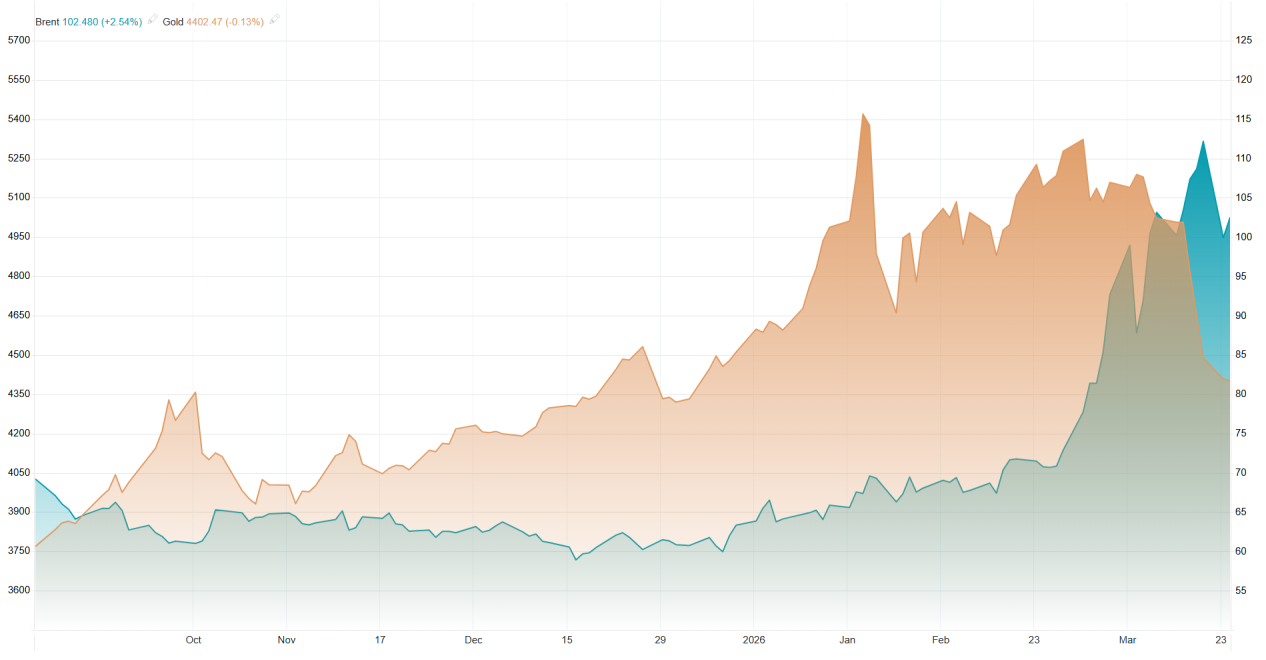

Based on in-depth analysis using ACE Markets’ global precious metals real-time monitoring system, central bank gold reserve tracking database, cross-asset pricing model, and institutional holdings analysis system, the gold market recently experienced historic extreme volatility, recording its largest single-week drop since the 1980s, hitting a low of $4098.60 per ounce at one point. Even though a V-shaped rebound to $4450 followed due to easing geopolitical tensions has fundamentally reversed the core driving logic of the market. As early as the end of January, after gold prices reached a record high, the ACE Markets precious metals research team used multi-dimensional models to capture risk signals of speculative market tops and weakening core support, accurately predicting the abnormal volatility and failure of gold’s safe-haven attributes, and sending early risk warnings to users.

A review of extreme market conditions in gold: its safe-haven appeal suffers a historic failure.

ACE Markets’ global precious metals real-time price monitoring system has captured the full picture of this round of gold price fluctuations: After reaching a record high at the end of January, gold prices have continuously lost upward momentum. Even with the continued escalation of geopolitical tensions in the Middle East, it failed to trigger traditional safe-haven buying of gold, resulting in an abnormal divergence in price movements that completely deviated from geopolitical risks. Subsequently, gold prices experienced a precipitous drop, marking the largest single-week decline in over 40 years. On March 23, prices even dipped to $4,098.60 per ounce during trading. Only five days after Trump announced a delay in the strikes against Iranian energy facilities did a rapid V-shaped rebound occur.

Alongside gold, the silver market also weakened, falling for four consecutive trading days and accumulating a nearly 20% drop from its March high. On March 23, spot silver plummeted to $60.89 per ounce, only half of its historical high eight weeks prior, indicating a significant technical breakdown. In this extreme market condition, gold has completely broken the traditional pricing logic of “escalating geopolitical conflicts and high inflation leading to higher gold prices.” ACE Markets’ cross-asset linkage model verification shows that traditional safe-haven assets such as US Treasury bonds and Treasury Inflation-Protected Securities (TIPS) also failed to attract capital inflows during the same period, with the 10-year US Treasury yield climbing to a multi-month high. The market trading logic has completely shifted from “safe-haven hedging” to “liquidity competition.”

Breakdown of the core drivers behind the sharp drop in gold prices

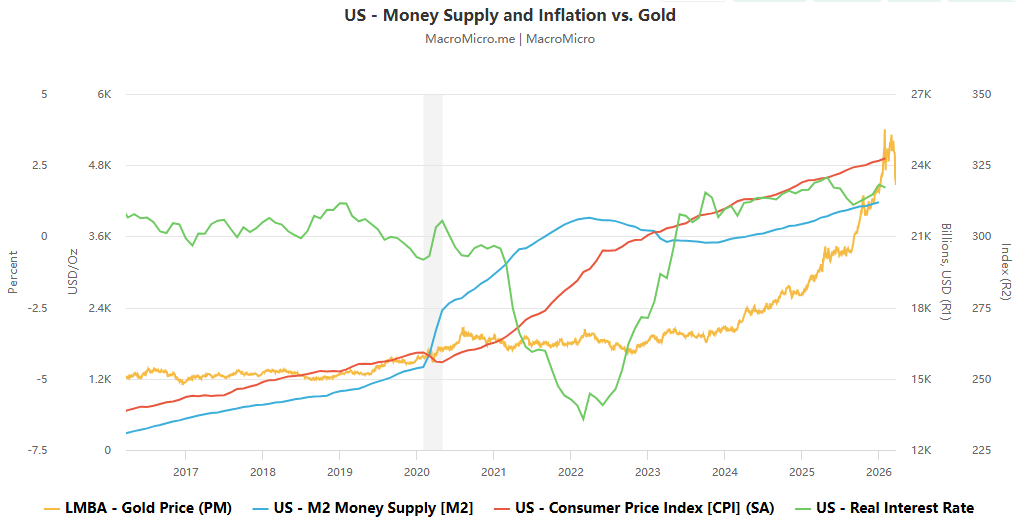

The core driver of gold price increases—central bank gold purchases—has completely reversed, with energy security taking precedence over reserve diversification. ACE Markets’ global central bank gold reserve tracking database shows that continuous central bank gold purchases since the end of 2022 have been the primary driver of rising gold prices. This support has now fundamentally reversed, a view strongly echoed by analysts such as Haworth and Dada. ACE Markets monitoring indicates that previously, the surge in gold prices was largely driven by central banks of net energy importers. Following the Iranian conflict, which pushed up energy and fertilizer costs, these countries have shifted their fiscal resources towards ensuring people’s livelihoods and energy supply, diverting funds originally intended for gold reserves. More alarmingly, ACE Markets analysis suggests that the recent gold price plunge may be accompanied by substantial selling by some central banks, aimed at defending their currencies or raising funds for energy purchases. This also explains the unusual phenomenon of the extreme drop in gold prices.

Rising real interest rates are suppressing gold valuations, with the dollar’s liquidity-siphoning effect dominating the market. ACE Markets’ interest rate-gold pricing model shows that the continued rise in nominal and real interest rates has significantly weakened the attractiveness of holding gold (a non-interest-bearing asset), which is the core macroeconomic driver of this round of gold price declines. Haworth’s analysis is completely consistent with the platform’s model calculations—even with high inflation, TIPS cannot play a safe-haven role; due to duration, rising real interest rates will simultaneously suppress TIPS and gold prices. Against the backdrop of geopolitical conflicts, market demand for safe-haven assets has shifted to a competition for dollar liquidity. Governments and companies are prioritizing the accumulation of dollars for energy procurement and supply chain maintenance, rather than increasing holdings of traditional safe-haven assets such as gold and US Treasury bonds. The dollar has become the sole core safe-haven asset, and its liquidity-siphoning effect continues to exacerbate the selling pressure on gold.

Speculative losses exacerbated liquidation pressures. ACE Markets’ institutional position monitoring showed that after gold prices hit new highs, speculative long positions were at historically high levels. The price decline led to substantial unrealized losses for speculative funds, forcing them to liquidate and further amplifying the drop. This aligns with Haworth’s analysis—most speculators were forced to liquidate and exit the market due to financial pressure. ACE Markets’ alternative asset monitoring module detected liquidity gaps in the private credit market in advance, a hidden driver of the extreme gold price decline. Data shows that in mid-March, several alternative asset management companies implemented redemption restrictions. Morgan Stanley North Haven only fulfilled 45.8% of redemption requests, and Cliffwater only honored half of the redemption applications. This is consistent with Solove’s assessment: redemption restrictions triggered margin calls, forcing investors to sell gold to cover debts, creating a negative cycle of “decline-liquidation-further decline.”

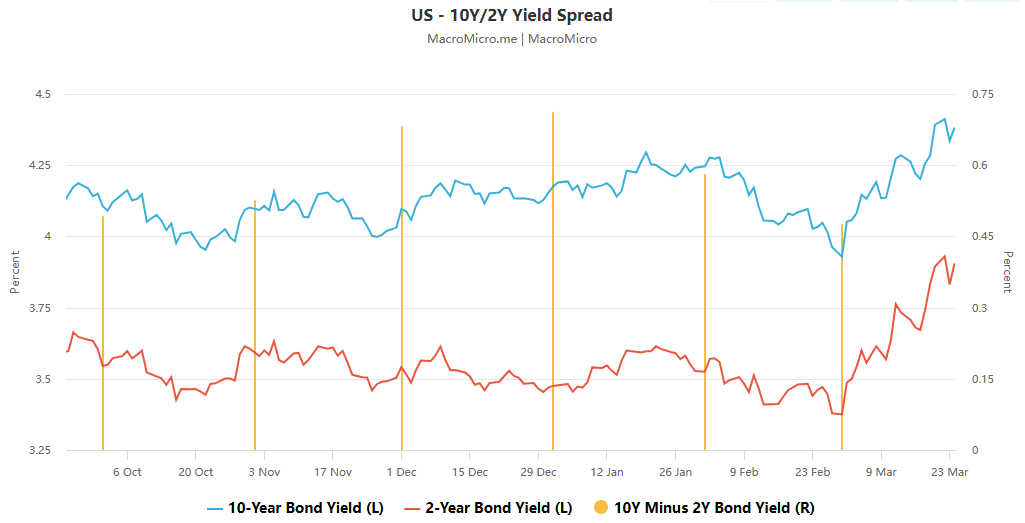

Volatility in US Treasury yields exacerbated valuation pressures on gold. ACE Markets fixed income monitoring showed that the 10-year US Treasury yield rose to 4.2% at one point, approaching the key threshold of 4.5%, exerting strong downward pressure on gold. This is entirely consistent with Solove’s assessment that “yield shocks dominate gold prices” and also highly aligns with the conclusions of the platform interest rate model. The analysis suggests that bond market volatility has begun to dominate the direction of US foreign policy. It was the rapid surge in US Treasury yields that forced the US government to ease tensions with Iran through diplomatic dialogue. This shift directly triggered a V-shaped rebound in gold, but it did not change the core logic of the gold market: “the core drivers have not reversed.”

ACE Markets’ Core Market Analysis and Monitoring Guide

Based on cross-validation and analysis of multi-dimensional data, ACE Markets believes the gold market has entered a core driver resetting phase. The short-term rebound is merely a technical correction driven by easing geopolitical tensions and is unlikely to reverse the downward trend. A return to an upward channel is only possible after a substantial reversal of core support levels. The sustainability of the short-term rebound is questionable, and further downside potential remains. Three core risks exist: the ongoing conflict in Iran will exacerbate fiscal pressure on central banks of energy-importing countries, making it difficult to resume gold purchases and potentially leading to further selling; the private credit liquidity crisis remains unresolved, and repeated liquidation and selling may occur; and the US Treasury yield exceeding 4.5% will further suppress gold valuations. Combining institutional views and platform model calculations, the short-term support level for gold is $4000/ounce, and in extreme cases, it may test $3500 (the key resistance-to-support range in April 2025).

ACE Markets believes that the long-term upward trend of gold has not fundamentally changed, and the current decline and liquidation are prerequisites for gold prices to move to higher levels in the long term. The platform’s analysis aligns closely with Solove’s “Phoenix Effect”: once the market liquidity crisis clears, geopolitical conflicts ease, and energy prices fall, central bank gold purchases will quickly resume. Coupled with a weakening dollar and the resumption of the Fed’s interest rate cut cycle, gold will experience a rapid rebound, likely returning to above $5,000/ounce within 3-6 months, with further potential to reach $10,000/ounce in the long term. Natixis’s view also resonates with the platform’s medium- to long-term analysis: if damage to energy infrastructure is limited and oil prices quickly fall back to pre-war levels, central bank gold purchases will significantly increase, pushing gold prices back into a sustained trading range above $5,000/ounce.

For market participants, relying on ACE Markets’ real-time monitoring system, they can focus on four key signals to grasp the turning points in the gold market trend: the subsequent evolution of the Middle East geopolitical conflict (especially the shipping situation in the Strait of Hormuz and the operating range of international oil prices, which are the core variables determining whether central bank gold purchases can resume), changes in global central bank gold reserves (focusing on the gold purchases and sales of net energy importers, which is the key to whether gold can regain its core support), the trend of the US 10-year Treasury yield and the Fed’s monetary policy statements (paying attention to the direction of changes in real interest rates, which is the core macroeconomic factor determining gold valuation), and the liquidity situation in the private credit market (tracking marginal changes in redemption restrictions and margin calls, and being wary of a new round of selling triggered by a liquidity crisis).