International capital bets on the real economy, while government bonds are in trouble: the core contradictions and future variables of Japan’s market differentiation

- August 29, 2025

- Posted by: Ace Markets

- Category: Financial News

Against the backdrop of intensifying global geopolitical uncertainty and persistent inflationary pressures, the Japanese market has recently exhibited distinct divergent characteristics: on the one hand, Berkshire Hathaway, owned by international investment giant Warren Buffett, has continued to increase its holdings in Japanese trading companies, signaling its long-term confidence in the real economy; on the other hand, the Japanese government bond market has been mired in controversy over a “value trap,” with overseas investors going from optimistic bets to losses. Coupled with the Bank of Japan’s ambiguous policy signals and rising market expectations of interest rate hikes, short-term bond auctions have been met with a cold reception, and the overall bond market is facing multiple pressures.

International capital’s confidence in Japanese trading companies: Berkshire Hathaway continues to increase its holdings

Berkshire Hathaway has increased its stakes in Mitsubishi Corporation and Mitsui & Co., two Japanese trading companies, directly driving up the overall share price of the Japanese trading company sector. Specifically, Mitsubishi Corporation stated in a statement on Thursday that Berkshire Hathaway’s subsidiaries have increased their voting stake in the company from 9.74% in March to 10.23%, breaking the previously implicit 10% ceiling. Mitsui & Co. also disclosed an increase in its stake, providing room for Berkshire Hathaway’s long-term investment strategy. This adjustment stems from Buffett’s initial plan, stated in his February annual letter to shareholders, to hold no more than 10% of the company.

The market reacted positively to this signal. After the Tokyo stock market reopened at noon, Mitsubishi Corporation’s share price rose as much as 2.9%, its biggest gain in three weeks; Mitsui & Co.’s stock price rose as much as 1.8%. Furthermore, three other major Japanese trading companies, in which Berkshire Hathaway has held positions since 2020, also benefited. These diversified trading companies, with businesses ranging from overseas oil and gas exploration to salmon farming to convenience store operations, are more actively increasing shareholder returns through stock buybacks and other means, making them attractive long-term investments amid geopolitical turmoil.

The Dilemma of the Japanese Government Bond Market: From a Guaranteed Profit to a Value Trap

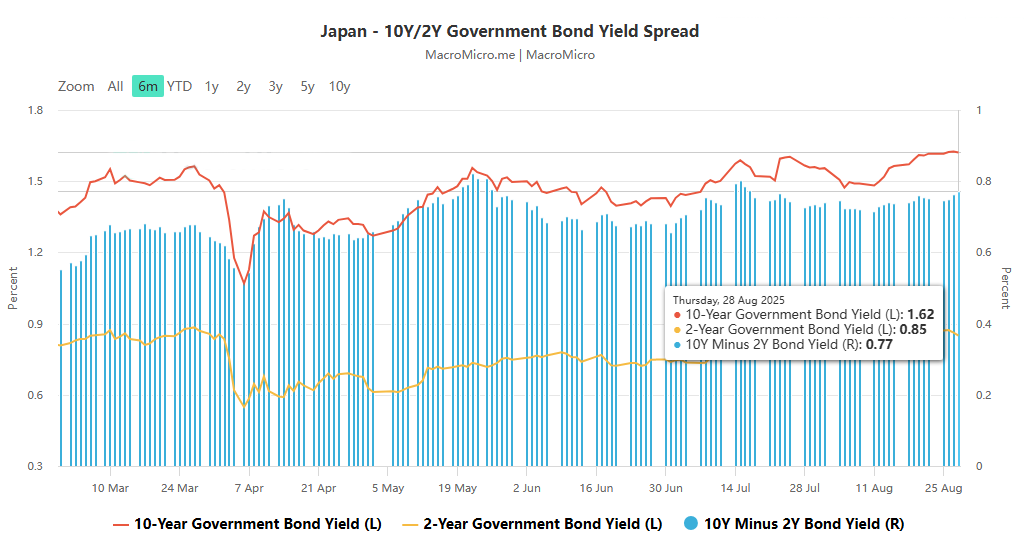

In contrast to the solid performance of the trading company sector, the Japanese government bond market (the world’s third-largest bond market, after the United States and China) has recently been caught in a period of sharp volatility. The “low-risk, high-return” strategy previously bet by overseas investors has suffered a heavy blow, and the market controversy over its “value trap” has gradually heated up.

This pressure comes from multiple dimensions:

- Central bank policy shift : After the Bank of Japan abolished the yield curve control (YCC) policy that it had maintained for many years, the global interest rate “anchor” was broken. The central bank not only delayed raising interest rates but also gradually reduced the scale of government bond purchases, weakening the key support of the market .

- Fiscal concerns intensify : After Japan’s ruling coalition lost the Senate election in July, market expectations for the government to launch a new round of fiscal stimulus have increased, triggering concerns about the expansion of government bond issuance, further suppressing bond prices .

- Shrinking domestic demand : Pension and life insurance institutions, which serve as the “ballast” of Japanese government bonds, have seen a decline in demand for ultra-long-term government bonds to match long-term liabilities due to an aging population .

- Global sell-off : Global bond markets have been hit by a sell-off due to high inflation and fiscal pressure. Japanese government bonds are not immune to the impact, and the buying power of overseas funds has slowed significantly .

Central bank policy and market game: short-term bonds cool amid interest rate hike expectations

- Amidst the sluggish bond market, market sentiment is sharply divided. Fluctuations in the Japanese government bond market are closely tied to the Bank of Japan’s policy signals and market expectations of interest rate hikes. Despite recent cautious signals from central bank officials, market bets on rate hikes have continued to mount, directly reflected in the lukewarm reception of short-term bond auctions.

- In her speech on Thursday, Bank of Japan board member Junko Nakagawa mentioned the possibility of raising interest rates and adjusting easing measures after meeting the target, and emphasized trade uncertainties to avoid expectations of rate hikes. The core of the speech was to stabilize the market before the September meeting, an attitude consistent with that of Bank of Japan Governor Kazuo Ueda. The US Treasury Secretary criticized the Bank of Japan for its “lagging action” in fighting inflation, further pushing up market expectations of rate hikes. Currently, traders believe that the probability of a rate hike before the end of October is about 60%. Japan’s 10-year government bond yield has risen to a 17-year high. The expectation of a rate hike also led to the weakest demand in 16 years for Thursday’s two-year government bond auction, and all government bond auctions this month were poor. The market believes that this reflects weaker demand and predicts that the yield curve will steepen and the long end will be under double pressure.

Summary: Differentiation of the Japanese market and key variables in the future

The current Japanese market presents a dual picture of “real industries are favored and financial markets are under pressure”: Buffett’s increased holdings in Japanese trading companies represent international capital’s long-term recognition of Japan’s diversified real business and optimized shareholder returns; while the difficulties in the government bond market expose Japan’s challenges in inflation control, fiscal balance and central bank policy transformation.

In the future, the direction of the Japanese market will be highly dependent on three major variables:

First, the Bank of Japan’s pace of interest rate hikes – if persistently high inflation forces a policy shift, it could reshape government bond market expectations;

The second is the effectiveness of business optimization in the trading company sector – whether it can continue to maintain its attractiveness through asset consolidation and repurchases;

The third is the trend of global capital flows – if the global bond market sell-off eases, it may provide Japanese government bonds with some breathing space.

For investors, the Japanese market presents both “differentiation opportunities” and “potential risks,” and they need to closely track changes in policy signals and macroeconomic data.