A Panoramic View of the US Economy from CPI to Debt: Inflation Divergence, Policy Gambling, and Debt Pressure Intertwined

- August 18, 2025

- Posted by: Ace Markets

- Category: Financial News

In July 2025, the United States released an intensive amount of economic data. The fluctuations in CPI inflation data, the chain reaction in the financial market, the divergence in the Federal Reserve’s policy expectations, and the continued expansion of the fiscal deficit together outlined a complex picture of the current economic operation.

1. CPI data fluctuated beyond expectations, and the market reacted sharply

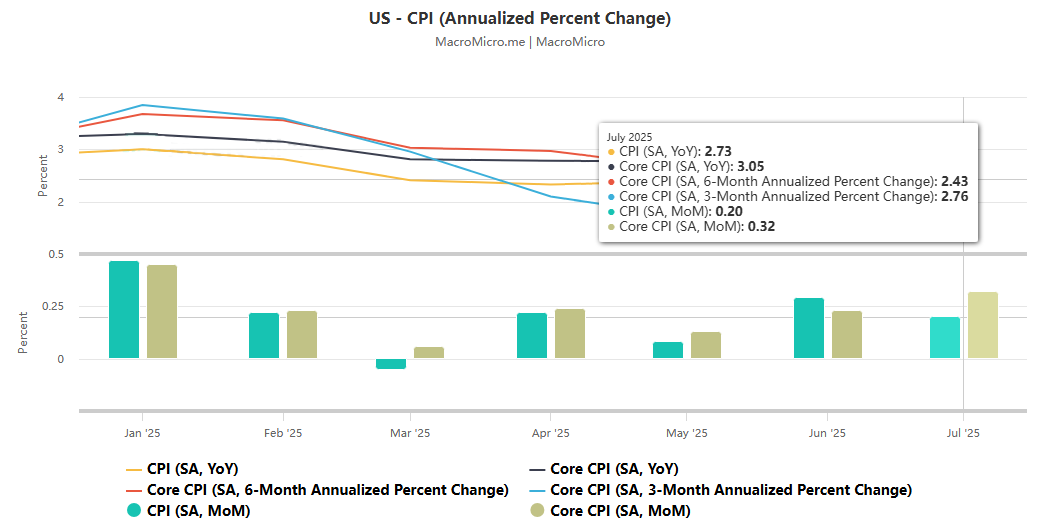

July’s US CPI data showed a divergent pattern of “strong core inflation and weak overall inflation.” The core CPI, excluding food and energy, rose to 3.1% year-over-year, a five-month high and exceeding market expectations of 3.0%. The monthly core CPI climbed to 0.3%, the first time it has reached this level since January and 0.2% higher than the previous reading, indicating continued accumulation of core inflationary pressures. In contrast, the headline CPI came in at 2.7% year-over-year, below expectations of 2.8% and unchanged from the previous reading. The monthly CPI of 0.2% was in line with expectations but down from 0.3% in the previous reading.

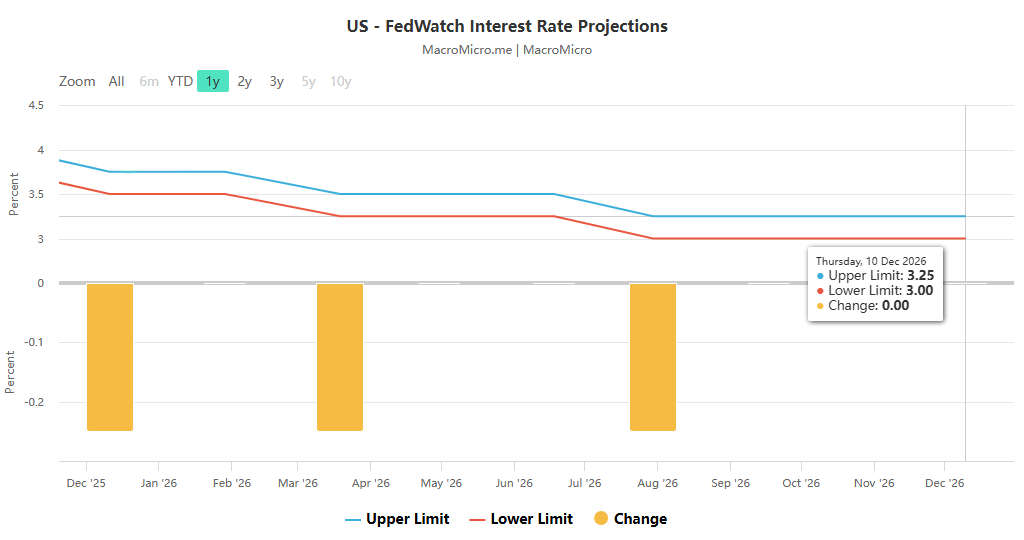

The release of the data instantly roiled financial markets: spot gold briefly surged to a high of $3,354 per ounce, then rebounded after a sharp decline, ultimately settling at $3,351.21 per ounce. The US dollar index briefly fell over 30 points, while non-US currencies generally rallied. The British pound broke through 1.35 against the US dollar, the US dollar fell below 148 against the Japanese yen, and the euro rose nearly 50 points against the US dollar. US short-term interest rate futures fell, as traders increased their bets on a September rate cut by the Federal Reserve, while maintaining expectations of a December rate cut.

2. Inflation drivers are complex, with tariffs and “super-core services” becoming the focus.

The structural characteristics of inflation were particularly prominent in July. “Super-core services” (excluding housing, commodities, food, and energy), a key focus of the Federal Reserve, rose 0.48% in July, the largest increase since January. Airfares surged 4% (the highest in over three years) and dental services rose 2.6% (a record high), contributing significantly to core inflation. The impact of tariffs on prices continued to be felt. Prices of household goods, impacted by tariffs, rose 0.7% on the month. While the pace of increase slowed, the 2.4% year-on-year increase still reached a two-year high. Video and audio product prices rose 0.8% on the month, and the 0.4% year-on-year increase was the largest since 2021.

Institutions such as the Canadian Imperial Bank of Commerce predict that tariffs may further push up new car prices after the fall launch of new models, due to the combined effects of reduced inventory and the new tariffs. However, the rate of increase in clothing prices slowed to 0.1%, initially suggesting that the impact of tariffs on this sector may have slightly diminished. Notably, prices in areas of basic living, which Trump has repeatedly emphasized, have cooled: “Food for sale” saw a slight decrease of 0.1%, while energy prices fell 1.1%, with gasoline prices dropping 2.2%, easing some of the cost of living pressures on households.

3. Institutional differences intensify, and the Fed’s policy direction becomes the core concern of the market

Analysts and institutions differ significantly on their interpretations of the July CPI data. Analyst Anstey warned that the core CPI exceeded expectations for the first time in six months, urging caution against an inflation inflection point. The data could continue to exceed expectations, contradicting the 12-month inflation trend that Federal Reserve Chairman Powell is focusing on, and is not a positive signal.

Optimists, however, believe there’s still room for policy easing. Analyst Jersey noted that the overall monthly CPI data suggests PCE figures before the September Fed meeting could approach the 2% target, paving the way for a rate cut. CreditSights even predicts a 50 basis point rate cut in September, as the cooling labor market has become a core concern for policymakers.

4. Data credibility is questioned, and political factors are intervening in market pricing.

The July CPI report is unique in that it is the first inflation data released by the Bureau of Labor Statistics (BLS) since President Trump fired its director. This move has raised market concerns about the credibility of official data. Global investors rely on this data to price trillions of dollars in assets, and years of declining BLS survey response rates have cast doubt on its quality. Macquarie strategist Thierry Weitzman bluntly stated that suspicions of political manipulation of the data could directly distort market trends.

The fiscal deficit hit a new high, and debt pressure is approaching the critical point

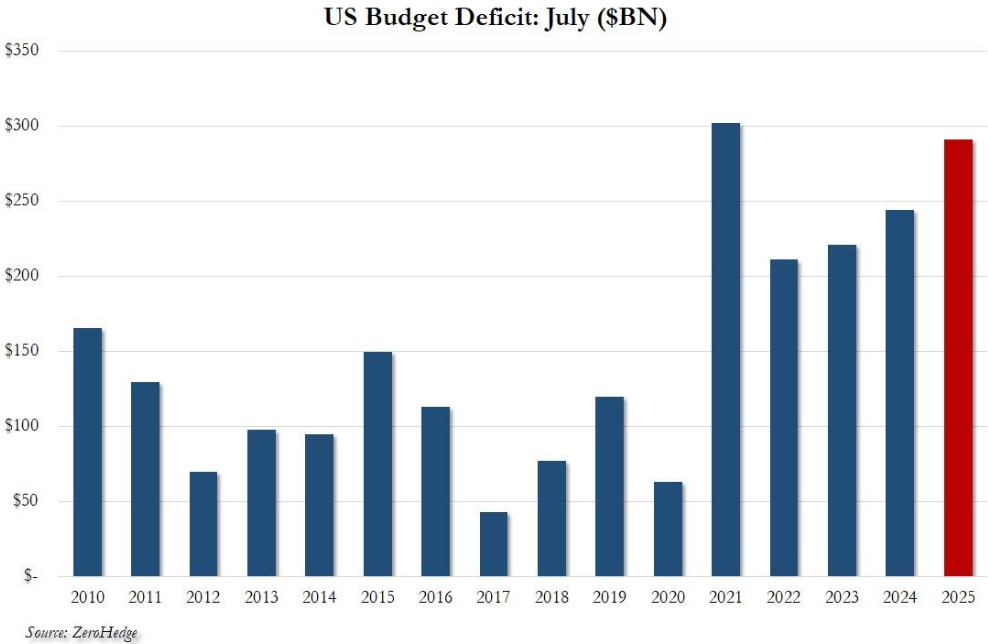

The fiscal report released alongside the inflation data cast an even more grim picture. U.S. federal government spending surged 9.7% in July to $630 billion, the second-highest amount since January. Revenue grew only 2.5% to $338 billion, including $19.3 billion in tariff revenue (excluding tariffs, revenue actually declined year-over-year). This imbalance caused the fiscal deficit to surge to $291 billion in July, a 20% year-over-year increase and the second-highest July deficit on record. As of July, the cumulative deficit for the current fiscal year reached $1.629 trillion, a 7.4% increase from the same period last year. Fiscal 2025 is likely to be the third-largest deficit year in U.S. history.

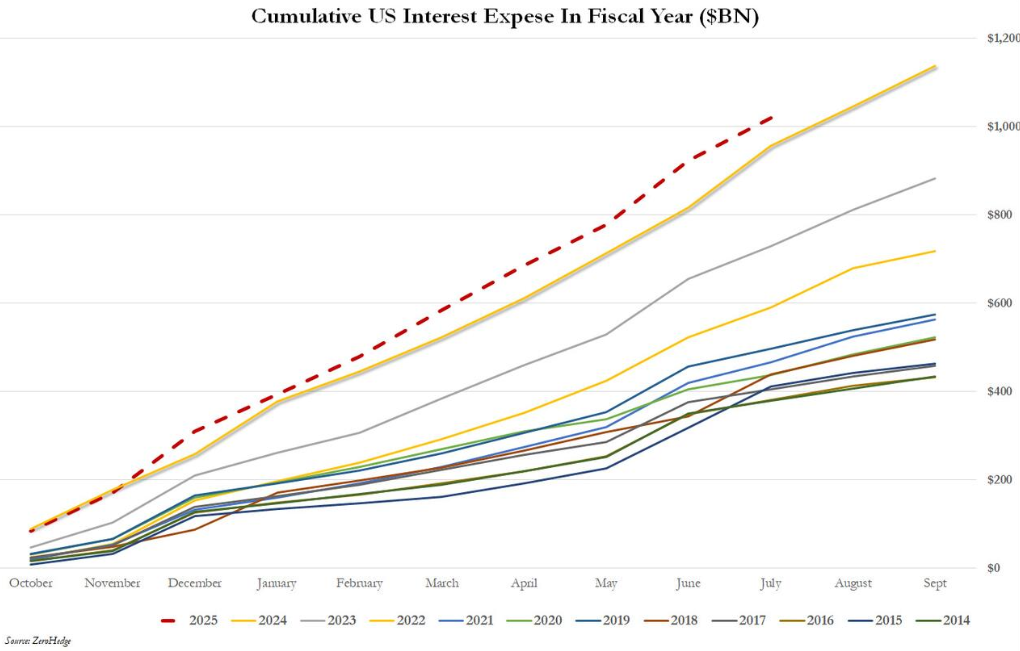

More seriously, the total U.S. national debt has surpassed $37 trillion for the first time, roughly 1.27 times the nominal GDP in 2024. Interest payments reached $91.9 billion in July alone, bringing the total for the first ten months to over $1.019 trillion and potentially exceeding $1.2 trillion for the entire year, firmly ranking it as the second-largest federal expenditure, behind only Social Security. Although tariff revenue has remained high for four consecutive months (approximately $19.3 billion in July, or an annualized $240 billion), this is a drop in the bucket given a nearly 10% increase in spending, making it difficult to reverse the deteriorating fiscal situation.

Conclusion

July data revealed multiple contradictions in the US economy: sticky core inflation coexists with cooling overall inflation; short-term price increases from tariffs intersect with long-term fiscal pressures; and the tussle between expectations of Federal Reserve rate cuts and inflation risks persists. These contradictions not only influence short-term fluctuations in financial markets but also foreshadow the complexity of future economic policy adjustments. Finding a balance between curbing inflation, stabilizing employment, and mitigating fiscal risks will remain a core challenge for the US economy.