Gold plunges 6% in a single day, hitting a 5-year high – short-term pressure vs. long-term bull market? Should you sell or buy now?

- October 23, 2025

- Posted by: Ace Markets

- Category: Financial News

1. Historic Plunge: Data and Background Describe the Full Impact

On Tuesday, October 21st, international gold prices experienced a precipitous drop. London gold futures plummeted from an all-time high of $4,381.52 per ounce, falling as much as 6.3% intraday to a low of $4,003.43 before closing down 5.3% at $4,123.85. December gold futures in New York plummeted 5.7% to close at $4,109.10, marking the largest single-day drop since April 2013 and the sharpest correction in nearly five years. Domestic markets also came under pressure, with the Shanghai Gold contract plummeting 4.81% and the Gold T+D contract plummeting 4.88%. Speculation of a “gold price crash” sparked panic on social media.

2. The Origin of the Plunge: The Resonant Release of Three Short-Term Factors

This plunge is not a signal of trend reversal, but the result of the combined effects of technical corrections, capital flight and macro disturbances, and has nothing to do with the long-term value logic of gold.

1. Technically overbought: a delayed valuation correction

This recent plunge stems from a divergence between asset prices and fundamentals. Gold prices saw a stunning surge in 2025, surging 25% in two months and $1,000 in six weeks, pushing technical indicators like the RSI into overbought territory. Nicky Shiels, Head of Metals Strategy at MKS PAMP SA, noted that such gains have made gold prices significantly overvalued, making a correction inevitable. Market dynamics indicate that a correction after an overbought period is a normal process of profit-taking and market correction.

2. Capital Stampede: Profit-taking rallies

The massive concentrated selling of profit-taking in the previous period significantly amplified the decline. From 2023 to 2025, the gold price doubled from 452 yuan/gram to 973 yuan/gram, bringing substantial returns to investors. After reaching a record high of $4,381, short-term speculators cashed in their profits, and fund managers followed suit, reducing their holdings, triggering a chain reaction of selling. Chandler of Bannockburn Capital Markets analyzed that the plunge stemmed from fear of loss (FOMO) funds being forced to liquidate their positions. Furthermore, the end of India’s Diwali gold-buying season led to a temporary cooling of physical demand, resulting in insufficient market capacity and further exacerbating selling pressure.

3. Macroeconomic disturbances: US dollar rebound and sentiment shift

Short-term changes in the external environment have become a catalyst for the plunge:

- Dollar rebound suppresses : The US dollar index is negatively correlated with gold. Recently, the ICE dollar index rebounded to around 99. The cost of purchasing gold for non-US currency holders has increased, suppressing gold prices.

- Risk aversion is receding : As the Sino-US trade situation eases, a large amount of safe-haven funds are withdrawing from the gold market.

- Data gaps exacerbate volatility : The U.S. government shutdown has led to the suspension of the CFTC’s position report, making it difficult to judge institutional positions and making it easy for speculators to build unilateral positions, amplifying market volatility.

III. Market Outlook: The Game Between Short-Term Repair and Long-Term Logic

The market’s disagreement on the future trend of gold is essentially a difference in perception of short-term fluctuations and long-term trends.

1. Short-term: Oversold rebound is more likely, with $4,000 becoming the key support

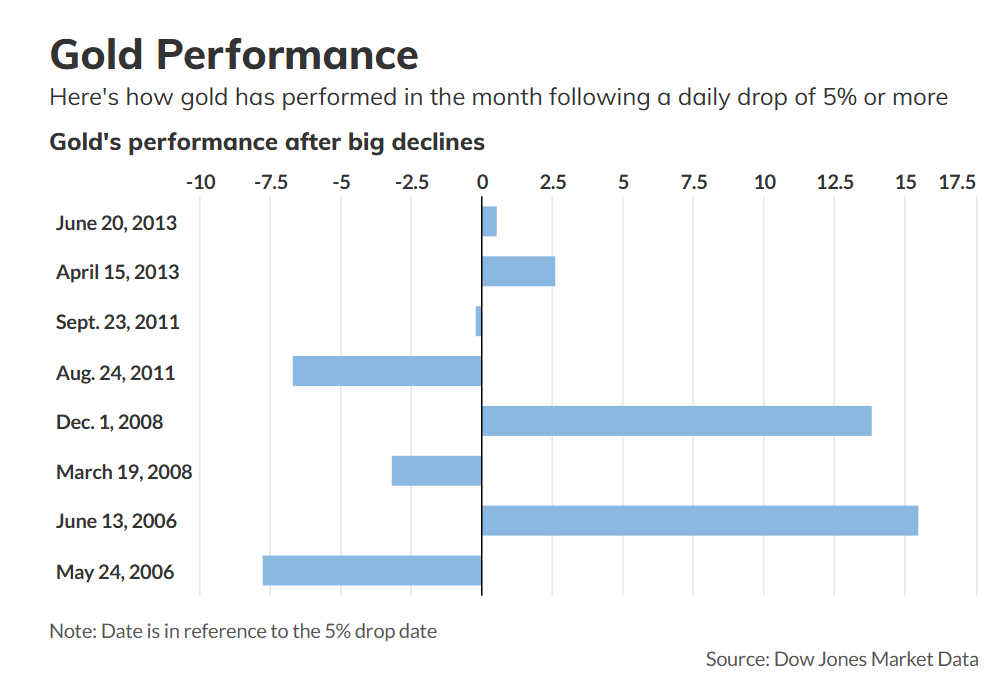

Historical data shows that single-day gold price drops of more than 5% are often unsustainable. Dow Jones data indicates that since 2006, such sharp declines have been followed by an average monthly gain of 1.82%. For example, in June 2006, gold prices fell 7.3%, only to rebound 15.46% the following month. Currently, London gold has rebounded from a low of $4,003 to $4,112.21, while New York gold has rebounded to $4,123.7. Strong support around the $4,000 mark is driving bargain-hunting funds into the market. StoneX analyst Fawad Razaqzada points out that $4,150 is a key level; a break above it could restart the upward trend, while a break below $4,000 could signal a new round of correction.

2. Long-term: The core support remains unchanged and the bull market foundation is still there.

Most institutions believe that the structural logic supporting the rise of gold has not been shaken by the short-term plunge:

- The foundation of safe-haven demand is solid : global economic and financial risks continue to rise, the size of the US private credit market exceeds US$1.7 trillion, household debt has hit a historical high of US$18.4 trillion, and credit card delinquency rates continue to rise, providing long-term safe-haven support for gold.

- Central banks continue to purchase gold : In the first half of 2025, global central banks made a net purchase of 500 tons of gold, a year-on-year increase of 25%. Official reserve demand has become an important support for gold prices.

- Positive policies and expectations : The market anticipates three Federal Reserve rate cuts totaling 75 basis points in 2026, maintaining the long-term weakening trend of the US dollar. Goldman Sachs raised its gold price forecast for the end of 2026 to $4,900, believing that demand for diversified allocations will drive gold prices to new highs.

3. Key disagreement: Can the logic of “devaluation transaction” continue?

The biggest controversy in the current market is centered on the effectiveness of the popular “dollar devaluation trade” in 2025:

- Bullish : Stefan Gleason, president of the Currency and Metals Exchange, believes that the pullback is “healthy and beneficial,” that the bull market was “born on a wall of worry,” and that it is “extremely foolish” to assert that the devaluation trade has failed simply because of a short-term plunge. The logic of long-term dollar devaluation still holds true.

- Skeptics : Chandler pointed out that the US dollar is still overvalued (the euro and the yen are undervalued by more than 50% relative to the US dollar). Even if it returns to fair value, it “cannot be considered a real devaluation” and the devaluation transaction lacks core basis.

IV. Conclusion: Rational Choices in Fluctuations

This recent gold plunge is essentially a “bull market shakeout” rather than a sign of a trend reversal. For long-term investors, the current 8.6% correction is close to the historically normal range of corrections, and the $4,000 level may present an opportunity for investment. Short-term traders should closely monitor the US dollar, Federal Reserve policy signals, and fund movements following the release of CFTC position data. As history has shown, gold, as a cyclical asset, has a true value that lies not in single-day fluctuations but in its ability to preserve value and hedge against global economic uncertainty.