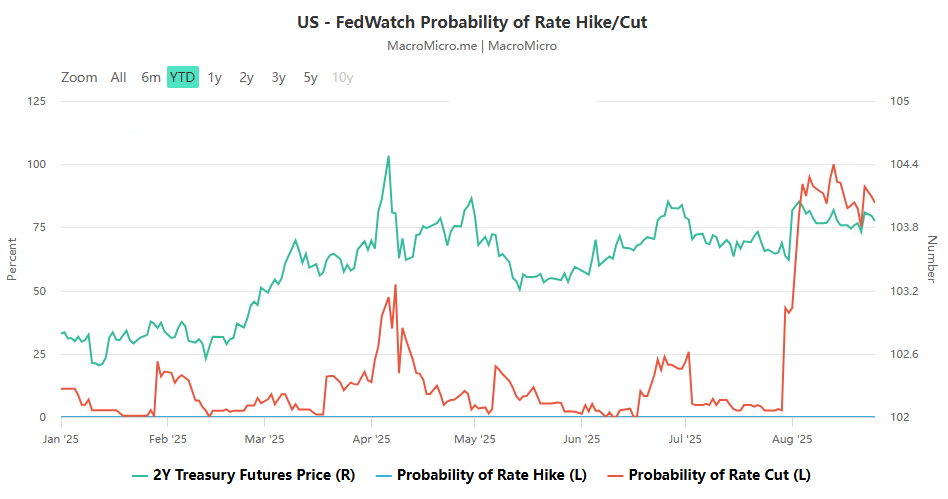

Powell bets on interest rate cuts to stabilize employment, and the August non-farm data becomes the “first touchstone” !

- August 26, 2025

- Posted by: Ace Markets

- Category: Financial News

At the Jackson Hole, Wyoming, global central bank symposium last Friday, Federal Reserve Chairman Powell signaled a rare September interest rate cut, the first in nearly a year. The key reason for this move is significant volatility in the US labor market and the need to balance inflation risks. This rate cut is seen as a policy measure to “support the labor market with low interest rates and prevent runaway inflation.” August’s non-farm payroll data will be crucial in determining whether the September rate cut will materialize and the pace of subsequent policy changes.

1. The core background of the interest rate cut signal: Intensified concerns about the labor market

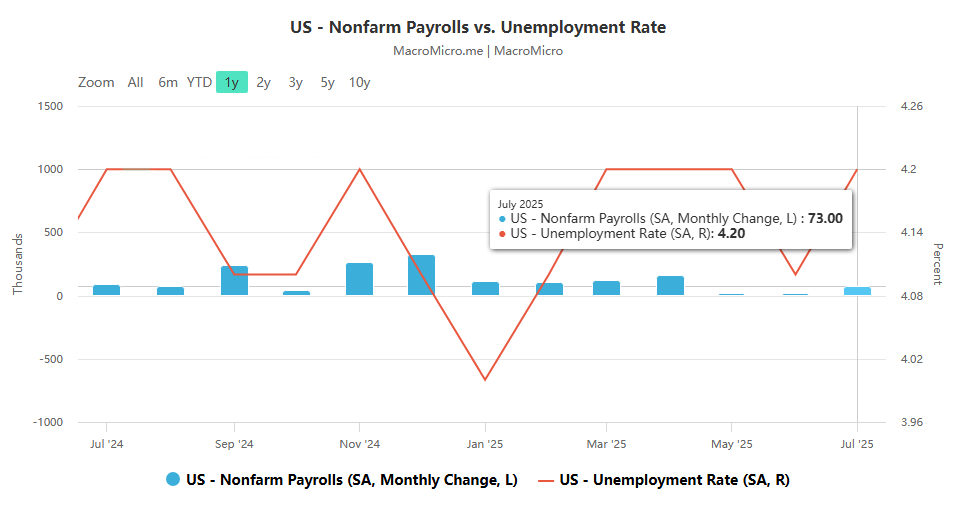

- Key data triggered the shift : July’s US non-farm payroll report was significantly revised downward, with weaker-than-expected job growth in May and June. After the revision, the US economy has added only 35,000 jobs per month since June, far below the 168,000 monthly average expected in 2024. This data sent shockwaves through the market, even leading to Trump’s dismissal of the Labor Department’s chief statistician and becoming a key turning point for Powell, who opened the door to interest rate cuts.

- The labor market is declining in multiple dimensions :

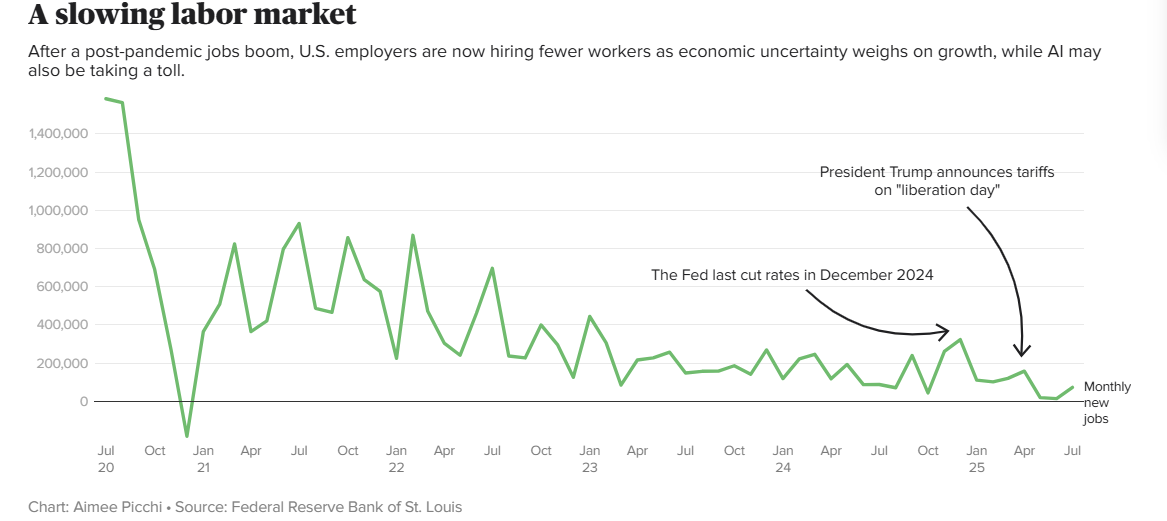

- Corporate hiring is shrinking : The average monthly number of new jobs added by U.S. employers in 2025 will be significantly lower than the post-epidemic economic rebound period. Due to the impact of tariff policies, the application of artificial intelligence and economic uncertainty, companies have generally postponed hiring. Some companies have also revealed that they may lay off employees in the future. Andy Challenger of the executive outsourcing firm Challenger, Gray & Christmas bluntly stated that “the labor market is indeed cooling, and there are more reasons for pessimism than optimism.”

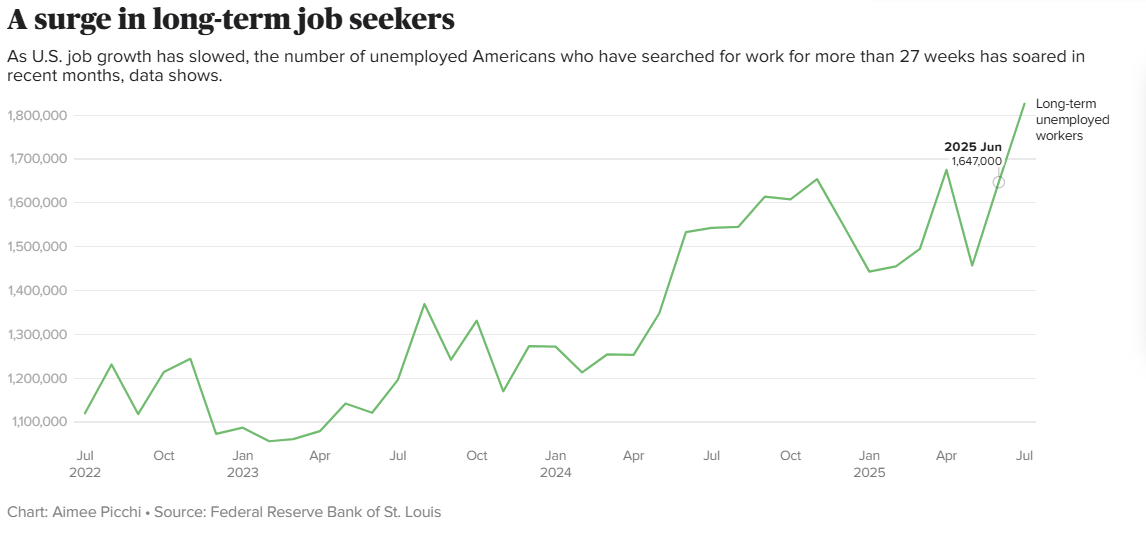

- A surge in long-term job seekers : In July, there were approximately 1.8 million long-term unemployed people who had been looking for jobs for more than 27 weeks, an increase of 64% from three years ago and 20% from a year ago. Due to the expectation of corporate layoffs, the difficulty of finding a job is unlikely to ease in the short term.

- Young people are finding it increasingly difficult to find jobs: New entrants to the labor market, such as recent graduates (mostly college and high school students), are finding it increasingly difficult to find their first job. In July, the proportion of new entrants in the total unemployed population rose from 1/12 in 2022 to 1/7. This is due to factors such as the economic slowdown and the replacement of entry-level jobs by artificial intelligence. Career coach Tracy Newell calls this “a perfect storm for employment” for graduates, with companies restricting entry-level positions and fierce competition for applications.

- The Federal Reserve’s policy trade-off : The Fed shoulders the dual mandate of curbing inflation and preserving employment. The White House’s tariff increases inherently create a dilemma: rising inflation and a weak economy. The logical precedence should have been to prioritize controlling inflation and maintaining high interest rates. However, Powell stated that the labor market urgently needs “urgent assistance,” warning that if downside employment risks materialize, they could trigger “a surge in layoffs and a surge in unemployment.” Furthermore, the Fed’s current inflationary risks are manageable (there are no significant signs of a “wage-price spiral,” labor shortages caused by immigration restrictions are limited to a few industries, and there are only weak signs of accelerating overall wage increases), providing confidence for a rate cut.

2. August non-farm payroll data: the decisive factor for a September rate cut

- Unprecedented Data Weight : After Powell signaled a rate cut, the market clearly identified August’s non-farm payroll data as the key determinant of a September rate cut. The Goldman Sachs team noted that if August’s non-farm payroll figures fall below 100,000, a September rate cut would be a near certainty. Their August forecast of 80,000 new jobs, combined with the previous monthly average of 35,000 in March, would exceed the “balanced growth” threshold for the job market and confirm a slowing trend.

- Data accuracy is in doubt : Goldman Sachs warns that current employment data may be subject to multiple risks of overestimation, including the “birth-death model” exaggerating the actual employment scale, the divergence between ADP data and official medical industry employment data, and the deviation of household surveys in immigrant employment statistics.

- Structural reasons for the slowdown in employment : The weakening of employment growth is not only due to trade and immigration policies, but also because the “catch-up hiring” (filling the labor gap in some industries) that previously supported the data has ended in many fields, and employment growth in the remaining industries has almost returned to zero, which is consistent with the overall economic activity slowdown trend in 2025. The Federal Reserve is worried about “acting too late and missing the window for stabilizing employment.”

III. Uncertainty about the pace of subsequent interest rate cuts and policy coordination

- The pace of interest rate cuts depends on the unemployment rate : Even if the interest rate cut is implemented in September, the pace of interest rate cuts in the rest of 2025 and 2026 will be determined by changes in the unemployment rate in the coming months. Barclays senior economist Jonathan Miller believes that the continued rise in the unemployment rate may lead to more radical interest rate cuts, and policies will gradually return to normal once employment stabilizes. Powell will stick to the position of “interest rate cuts, not economic stimulus” because the current interest rate range of 4.25%-4.5% is still above the neutral level of the economic cycle, and the interest rate cut is a “correction of the previous tight policy.”

- Policy connection in the “post-Powell era” : Goldman Sachs predicts that regardless of whether the economy slows down or normalizes, this round of interest rate cuts will most likely have ended when the next Federal Reserve Chairman takes office. The current interest rate cut is not only to respond to short-term employment risks, but also to pave the way for subsequent policy connections.

In summary, the current U.S. short-term interest rate market is in a wait-and-see state of “waiting for the August non-farm payroll data.” Although Powell has given the green light for a September rate cut, the policy game of “balancing employment and inflation” still needs to use the August non-farm payroll data as the first key footnote, and the medium- and long-term policy direction is still deeply affected by labor market dynamics and economic trends.