Will the Middle East conflict drag down the US stock market? Three supporting factors provide the answer !

- April 8, 2026

- Posted by: ACE Markets

- Category: Financial News

Recently, amid concerns about the potential impact of escalating geopolitical tensions in the Middle East on US stocks, extremely pessimistic “Willie’s Wolf moment” narratives have intensified, with many predicting a dramatic, unsupported plunge in US stocks, mirroring the cartoon character’s precipitous fall. However, the ACE Markets research team, based on comprehensive monitoring of geopolitical evolution, historical market patterns, US stock fundamentals, and core industry trends, believes that current pessimistic expectations are significantly overblown. While the tail risks of geopolitical conflict still warrant close attention, US stocks are not in a precarious position, and a market crash is not an inevitable outcome.

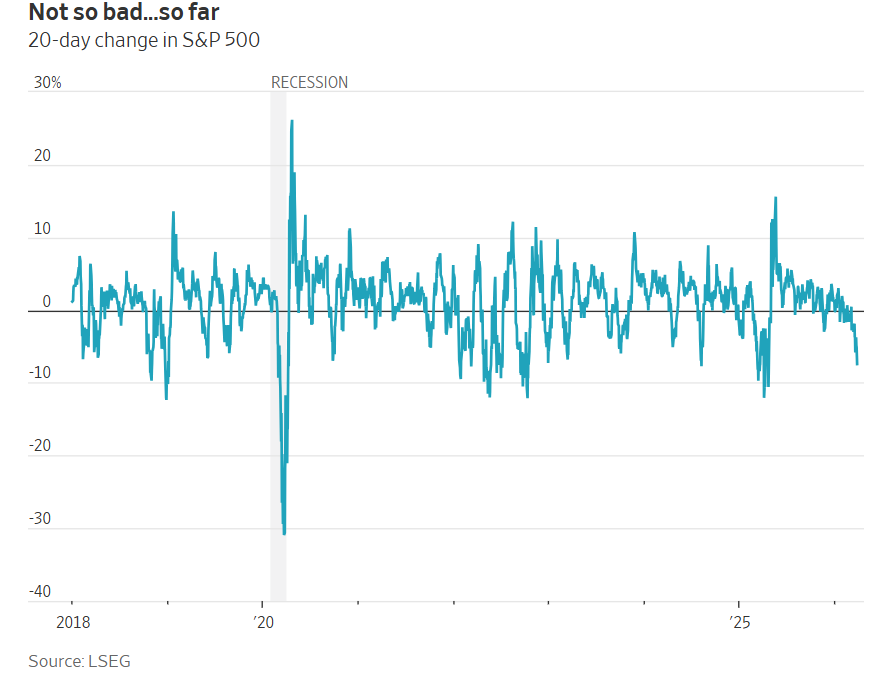

From the current market performance, even with the continued escalation of geopolitical turmoil in the Middle East, the correction in US stocks has been relatively manageable. Data from ACE Markets shows that the S&P 500 has only fallen 7.4% from its pre-escalation high. This pullback is only slightly larger than the normal market fluctuations in May 2019 and April 2018, both of which are considered fully digestible phases of volatility in the long-term trend of US stocks. Even though the current global energy crisis has led some Asian countries to implement fuel rationing, some market voices believe that investors are “overly complacent.” However, in our view, this performance is precisely a rational pricing based on historical patterns and fundamental support, rather than blind optimism.

A Historical Review of Geopolitical Conflicts: War Was Not the Core Driver of the US Stock Market Bear Market

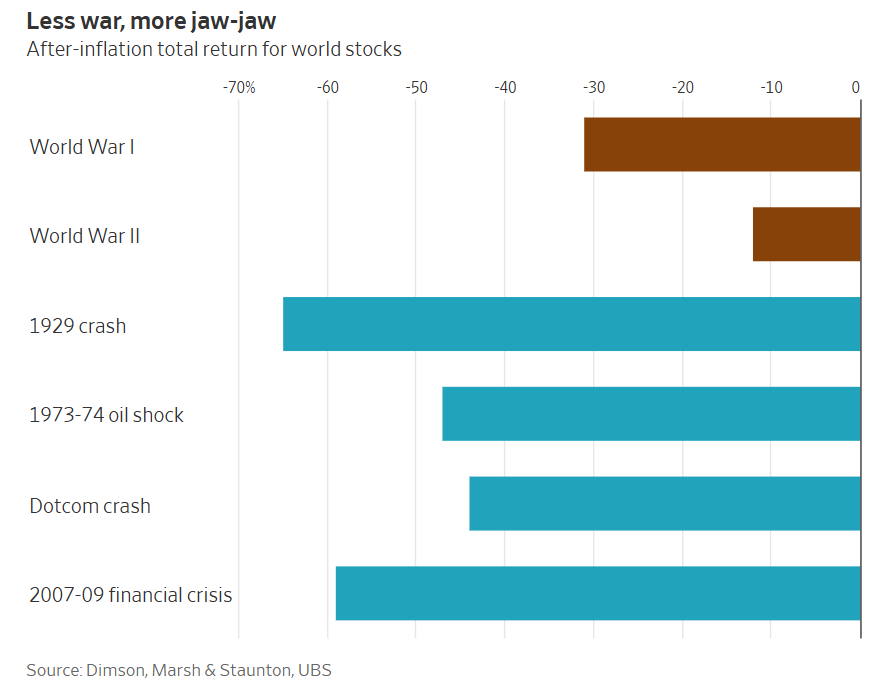

ACE Markets conducted an in-depth analysis of the market performance of 30 major global geopolitical events since 1939. The data confirms that military conflicts and geopolitical instability rarely have a sustained impact on the US stock market. After such events, the average decline in US stocks is only 4%, and they generally achieve a rapid rebound. The core underlying logic of this pattern lies in the fact that the US domestic industrial and economic foundation is rarely directly impacted by overseas wars. Even protracted wars like the Vietnam War and the Afghan War, which ended in US defeat, did not cause substantial damage to the US domestic industrial base. This is fundamentally different from the situation in countries like Britain, Germany, and Japan during World War II, where their domestic industries and cities were completely destroyed.

Furthermore, our analysis, combined with UBS’s long-term capital market research, further validates that the four major bear markets that have devastated global stock markets over the past century—the Great Depression, the 1973-1974 oil embargo, the bursting of the dot-com bubble, and the 2007-2009 global financial crisis—have had a far greater impact on the market than the two World Wars. Only countries whose domestic market foundations have suffered a systemic collapse have experienced devastating stock market blows during wartime; for example, the Russian stock market’s value plummeted to zero after World War I, and the Japanese stock market’s actual decline reached 96% after World War II. It is noteworthy that after the US invasion of Afghanistan in 2001, the US stock market initially rebounded briefly before falling into a year-long decline. The core driving factor was not the war itself, but the continued bursting of the dot-com bubble. This also confirms ACE Markets’ core analysis: the decisive factor in the US stock market’s performance has always been changes in the financial environment and economic fundamentals, rather than geopolitical events themselves.

Of course, the situation in Iran is unique—the Strait of Hormuz carries about one-fifth of the world’s oil shipments, and a blockade of the waterway would trigger a systemic gap in global oil supply. While spot oil prices have already risen significantly, futures market traders are still pricing in a price drop from the current $111/barrel to $85/barrel by the end of the year. In our view, this pricing reflects a rational expectation from the market regarding US policy intervention: with the midterm elections approaching, American voters have extremely low tolerance for high oil prices, and the Trump administration has repeatedly demonstrated its close attention to oil price trends. Whether it’s deploying troops to ensure the safety of the shipping lanes or pushing for a peace agreement, the policymakers have ample incentive to curb a prolonged, unilateral surge in oil prices.

Better-than-expected earnings fundamentals form a core safety cushion for US stocks.

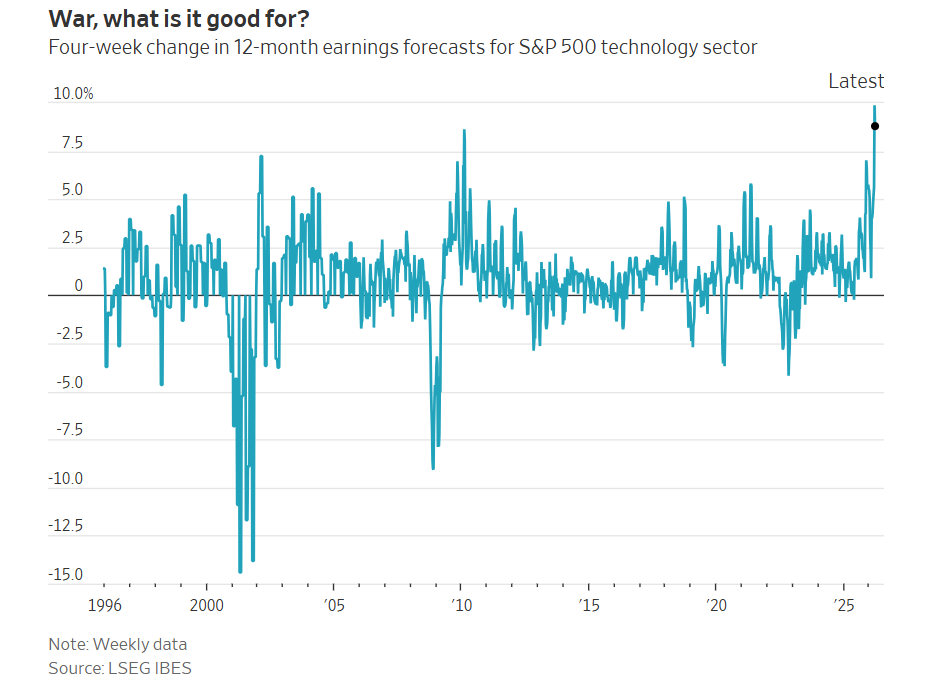

The resilience of corporate earnings is the core fundamental support for ACE Markets’ view that there is no need for excessive pessimism regarding US stocks. Our tracking of LSEG’s high-frequency earnings data reveals that since the initial strikes against Iran, the consensus earnings forecasts for S&P 500 components over the next 12 months have not only not been revised downwards with escalating geopolitical risks, but have instead risen against the trend. Wall Street’s expectations for S&P 500 earnings per share have cumulatively increased by 3.6%, marking the fastest short-term upward revision in five years. While the magnitudes vary slightly from other data sources, they all show a clear upward trend.

Looking at different sectors, the oil sector, benefiting from rising oil prices, naturally saw the largest increase in earnings expectations. However, the earnings expectations of other oil-consuming industries such as chemicals, aviation, and cruise lines were indeed impacted to some extent. But what exceeded market expectations was that since the escalation of the current situation, earnings forecasts for all sectors of the US stock market have been revised upwards, with the technology sector even recording its largest four-week gain since data became available in 1995.

Behind this better-than-expected performance lies the strong resilience of the US economy. ACE Markets assesses that although the US has become a net energy exporter, high oil prices will still have some impact on economic growth. However, prior to the outbreak of this round of geopolitical conflicts, the US economy was already in a strong operating range, possessing ample buffer space to absorb the mild impact of rising oil prices. Even with discussions in the market about stagflation, such as rising inflation and slowing growth, mainstream institutions have not included an economic recession in their baseline forecast scenarios. This is the core reason why corporate profit expectations can continue to be revised upwards. As we reached a consensus with global asset management firm Tikehau Capital: the global economy started the year on a solid foundation and is fully capable of absorbing this round of geopolitical shocks. If the crisis can be controlled in the short term, the economy and corporate profits for the whole year are still expected to achieve a solid performance.

Strong prospects for the AI industry continue to offset geopolitical uncertainties.

Optimistic expectations for the long-term development of the AI industry are another core force supporting the current valuation of US stocks, and this is also a key theme that ACE Markets continues to track closely. A major driver of this round of the US stock market bull run is the industrial revolution and capital expenditure expansion cycle brought about by the iteration of AI technology. Even against the backdrop of escalating geopolitical risks, investors continue to bet on a large influx of funds into core sectors related to AI, such as data centers and high-end chips. This expectation provides ample structural support and a psychological floor for the market.

Recent market volatility has fully demonstrated the core pricing power of the AI theme. A paper published by Google Research on a new data compression technology, proposing to reduce the demand for expensive short-term memory for large language models, caused the stock prices of companies such as SanDisk, Seagate Technology, Micron Technology, and Western Digital, which had previously surged due to soaring demand for high-speed storage chips, to plummet. In our view, this volatility precisely illustrates that the US stock market is currently highly sensitive to the technological iterations, supply and demand changes, and long-term prospects of the AI industry. The AI theme remains the core variable determining the structural trend of the US stock market, and its continued evolution will continue to bring incremental funds and valuation support to the US stock market.

Tail Risk Warning and Final Assessment

ACE Markets must point out that the effectiveness of the three supporting forces mentioned above is based on the core assumption that “the Middle East geopolitical conflict will end quickly.” This judgment still has the potential to be wrong: if Iran and the United States fail to reach an agreement on peace terms, if Israel continues to escalate the conflict, or if the United States intervenes militarily and becomes embroiled in a protracted resistance, leading to a prolonged disruption of the Gulf shipping lanes and even irreversible damage to oil production facilities, the global energy market will face a systemic shock. In the extreme scenario where oil prices soar to $200 per barrel, US stocks still face the risk of a significant correction.

Ultimately, the current market’s overhyped “Willie’s Wolf moment” is merely a low-probability, extreme tail risk, not a guaranteed baseline scenario. Investors’ cautious optimism towards US stocks is supported by solid historical patterns, better-than-expected corporate earnings, and the long-term development trend of the AI industry; it is not unfounded blind following. ACE Markets believes that emotional trading driven by geopolitical instability is often the core source of market misjudgments. Only through comprehensive data tracking, in-depth historical review, and rigorous fundamental analysis can we penetrate market noise and accurately grasp the core dynamics of asset prices—this is our consistent investment research principle.